Co-op Home Insurance Review 2026

Co-op Home Insurance Review 2026

Good for

- They've improved their cover recently

Bad for

- Hard to see exactly what's covered online or easily view a policy wording online.

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Cheap Home Insurance in Your Area

Quickly compare over 3 dozen UK insurance providers. Powered by QuoteZone.

Is Co-op home insurance any good? Quotes may seem competitive but there may be better home insurance companies out there.

In This Review

Co-op Home Insurance Review: What You Need to Know

Co-op Home Insurance may be competitively priced, but customer reviews aren't great and it's a bit hard to get a handle on their features, since policy wordings aren't readily available online, they work with a panel of underwriters, and they don't list coverage details on their website.

Co-op policies are primarily underwritten by a panel including West Bay Insurance Plc and Aviva Insurance Limited. Data from the latest FCA value measures (2024/2025) provides a clearer picture of their claims performance: West Bay typically accepts 80% to 85% of claims, while Aviva accepts 70% to 75%. Both underwriters perform at or above the industry average acceptance rate of 70.7%, offering reassurance regarding their reliability when a claim is filed.

While Co-op strives for competitive pricing, homeowners should evaluate quotes against the 2026 market average. As of early 2026, the average cost of a combined home insurance policy in the UK has risen to £356 per year for basic cover, while more comprehensive plans including accidental damage and home emergency cover now average £461 per year. These benchmarks are essential for determining if Co-op’s offers provide genuine value in a higher-premium environment.

We like that it seems there is some level of Accidental Damage cover included as standard to protect (as part of Contents cover) non-portable TV's, computers, DVD, AV equipment, fixed glass in furniture, fish tanks, mirrors and ceramic in hobs, plus (as part of Buildings cover) underground pipes, drains and cables, fixed glass, sanitary fittings, ceramic in hobs and solar panels. Accidental damage cover for events like wine spills on the carpet or drilling through a cable costs extra.

Co-op's optional Home Emergency cover costs around £40 per year. This price has increased from a few years ago, but so has their cover. Now call out charges are reimbursed up to £500 (it used to be just £250).

Co-op has a standard buildings replacement cost limit of up to £1,000,000, which has increased from £500,000 a few years ago. This limit will be more than enough for most people, but it depends on the rebuild cost of your home. While £1,000,000 is a substantial figure, it is worth noting that construction rebuild costs have risen by approximately 21% over the last two years. This surge makes it more important than ever for policyholders to accurately estimate their home’s rebuild value to ensure this £1,000,000 limit remains sufficient and avoids the risk of being underinsured.

Contents cover is available in an amount of your choosing up to £100,000.

Finally, you may find that Co-op won't quote you for home insurance. In the past, we tested out their website and found they were unable to provide quotes for some of our sample profiles. If you don't want to waste your time you might prefer to use a comparison site like our partner QuoteZone to get quotes from dozens of providers in just a few minutes.

Cheap Home Insurance in Your Area

Quickly compare over 3 dozen UK insurance providers. Only one form to fill out.

Co-op Home Insurance Key Facts

- One, simple plan

- Building rebuild cost maximum £1,000,000

- Contents cover up to £100,000

- Policies include some legal and limited accidental damage cover

- Can add more comprehensive Accidental Damage, Home Emergency and Personal Possessions cover

Optional Extras

To enhance your home insurance cover, you can add optional extras to a Co-op home insurance policy.

Home Emergency Cover: Home Assistance to help with emergencies such as boiler breakdowns (but they won't pay anything towards replacing a boiler), plumbing problems, loss of keys, pest infestation, etc. Maximum of £500 including VAT per event (this is consistent with many other major brands, although some pay up to £1,000).

Personal Possessions Cover: Protects your belongings that you take out of the house against loss, theft and accidental damage. Cover available from £2,500 to £20,000.

Enhanced Accidental Cover for buildings: e.g., DIY accidents like putting your foot through the attic floor or drilling through a pipe or cable.

Enhanced Accidental Cover for contents: e.g., paint spill on a new carpet or dropping an ornament. Note: damage by pets is not covered. In contrast, damage by pets is covered on Enhanced Accidental Cover with LV=. (Read our LV= home insurance review here.)

Co-op Home Insurance Customer Reviews, Complaints and Ratings

Co-op has earned 3.6 stars out of 5 by customers on Reviews.io, which reflects all of their insurance products including car, home, pet, travel, life, business, etc. We've scoured the reviews looking for comments on their home insurance specifically. Here are some real-life customer complaints (note, we saw a few related to a lack of documents in the post—when you get a quote they auto-select that you will receive documents online; if you wish to receive them by post, you'll need to change the selection on the quote form):

"Everything good but I don't have any documents by post."

"Despite no recent claims and a ncd of 40% I have been quoted a renewal figure in excess of £780 per annum for the same level of cover and they are unable to tell me the reason for the 150% plus increase."

"Had legal cover with home insurance but they would not allow us to claim and refused to send written details of why not, even though that is a legal requirement... We had consulted a barrister and had a high chance of winning the case but they were not interested and refused outright."

"Three weeks after we paid, Co-op cancelled our home insurance as we had "too many previous claims recorded with CUE" which we hadn't told them about. My wife had phoned the previous insurer a few times in the past for advice and every time it was recorded as a £0.00 claim."

"Read the small print first before you get a policy with co-op. Not like the old family orientated co-op used to be."

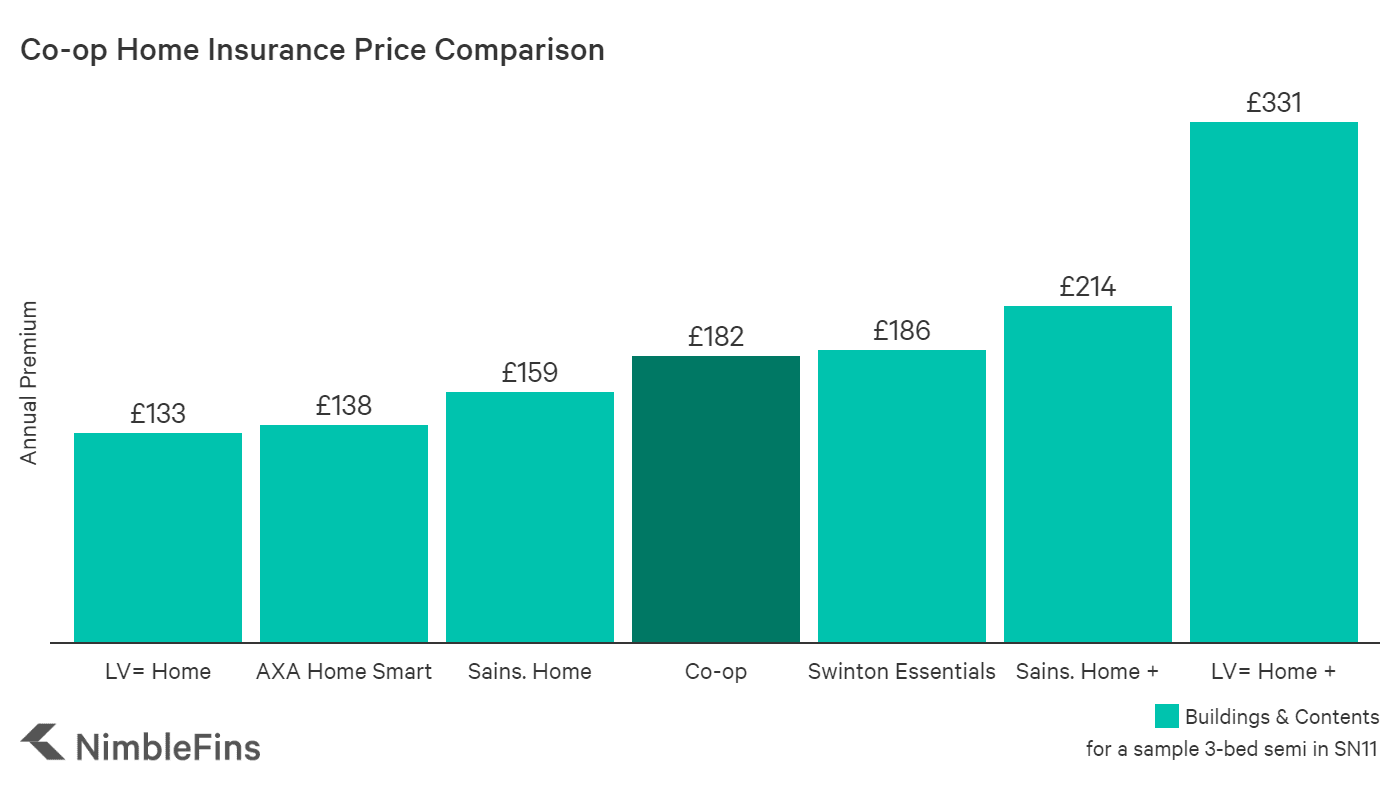

Co-op Home Insurance Price Comparison

We found that Co-op's home insurance policy starts off roughly low-to-mid market. Co-op plans do not include extended Accidental Damage, Home Emergency cover or Personal Possessions cover—adding some of these features (with £2k of Personal Possession cover) onto a basic policy increase your premium around £75+ the first year to £90-£100+ in subsequent years (due to HomeRescue discounts available the first year).

The chart below shows sample quotes for a 35-year-old policyholder living in a mortgaged, 3-bedroom property an SN postcode, who has 5 years of no claims. Insurance quotes can vary significantly from day to day and according to your individual details, so please just use the following data for educational purposes only; your quotes may reflect a large degree of variation. Policies below all have a £100 excess.

Co-op gives the option to choose an excess of £50, £100, £150 or £300. A policy with a higher excess will have a lower premium, because you're committing to pay more towards any valid claims. While a lower premium is certainly enticing, before signing up for a policy with a higher excess be sure you're able to cover the excess in the event of a valid claim.

Co-op Home (Buildings and Contents) Insurance Add-On Costs

Here are estimated costs of add-on extras for a mortgaged, owner-occupied, 3-bed property in an SN postcode when you buy an Co-op buildings & contents home insurance policy. It can be useful to have an idea of the approximate cost of these optional features when you're deciding what cover to buy.

| Co-op Home Insurance Extras | Rough Estimated Cost |

|---|---|

| Accidental Damage - Buildings | ~£30 |

| Accidental Damage - Contents | ~£20 |

| Accidental Damage - Buildings & Contents | ~£50 |

| Home Emergency Cover | nil (~£20 second year, ~£30 third year) |

| Personal Possessions (£2.5k) | ~£35 |

| Personal Possessions (£5k) | ~£50 |

Co-op Home Insurance Notable Exclusions

Co-op home insurance exclusions on the policy wording we examined include (but are not limited to) damage to fences, gates or hedges, loss or damage if you've been away for 60 days or more (occasional visits don't count), frost damage, damage by pets, subsidence (due to coastal or river erosion, settlement, faulty workmanship, etc.), etc.

A few exclusions stood out to us as particularly mentionable. You may want to keep them in mind if you go with Co-op or as you're comparing different home insurance plans. It's always a good idea to read through the full list of exclusions in the policy documents as we've only mentioned some exclusions here from the wording we examined and this may vary depending on the underwriter, and others may be more relevant to you that we have not mentioned.

- 1. For policies including Personal Possessions cover, theft from a vehicle is only included if the item is hidden from sight in a locked boot or a closed glove box, and the car doors and windows are securely locked—note, the policy documents do not specify a "theft from vehicle" limit (we frequently see a £1k or £2k limit from many other insurers).

- 2. Those who go abroad for more than 60 days at a time (perhaps to a second, holiday home) won't have cover for escaping water or oil, theft, vandalism, freezing of fixed water/heating system/fixed domestic appliance, fixed glass/sanitary fittings/mirrors, food in the freezer, contents in garden, etc.

- 3. Doesn't cover loss or damage during household removals to valuables/clothing or any loss or damage caused by theft/attempted theft unless access to from furniture depository gained by violent and forcible means.

- 4. Plants, trees and shrubs in the garden are not covered.

No Claims Discount

Co-op offers a No Claims Discount on Buildings and Contents insurance. Personal Possessions, Legal Expenses and HomeRescue Plus are not eligible for a No Claims Discount—this means that any claim you make under these areas of cover will not affect your No Claim Discount under Buildings and Contents. The Co-op NCD is subject to change but previously worked according to the following details:

| No Claims Discounts Scale | |||||

|---|---|---|---|---|---|

| NCD increases with each claim free year from Nil to: | 10% | 15% | 20% | 30% | 40% |

One claim will lose one year’s No Claim Discount (e.g., 40% drops to 30%, etc.), two claims will lose two years’ No Claim Discount (e.g., 40% to 20%, etc.) and three claims will reduce your No Claim Discount to Nil, regardless of your previous discount. Once you hit the maximum 40% No Claim Discount on either Buildings or Contents, you can request protection for your No Claim Discount for that section, for an additional cost.

Co-op Buildings & Contents Insurance: What's Covered?

Co-op cover protects against calamities such as fire, explosion, lightning, earthquake, smoke, frost, attempted theft, storm, flood, escaping water and oil, subsidence (depending on cause, etc.), etc. The exact cover may vary depending on the underwriter as they work with a panel, so it's important to check your offer documents.

Co-op Home Buildings Cover

- Rebuilding costs up to £1M

- Up to £2m property owner’s liability

- Alternative accommodation if your home can't be lived in due to an insured event up to £100,000

- Finding and accessing leaks up to £5,000

- Underground pipes, drains and cables up to £1 million

- Blocked drains up to £5,000

- Damage caused by emergency services up to £1,000

- Legal expenses up to £50,000

Co-op Home Contents Cover

- Contents loss or damage up to £100,000

- Food in the freezer up to £1,000

- Garden contents up to £1,000

- Home office equipment up to £10,000

- Personal money up to £500

- Lock replacement up to £1,000

- High risk items up to £3,000

- Student cover up to £5,000

- Bike cover up to £1,500 (per bike) and up to £3,000 (total)

- Theft from outbuildings up to £2,000

- Rent and alternative accommodation up to £20,000

- Legal expenses up to £50,000

- New for old replacement of items except household linen and clothes

FAQs

Other Useful Information

The Co-op home insurance policy wording used to be available here but now you must get a quote to get the policy wording. They work with a panel of insurers so the wording might vary from one person to the next.