The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

I'm a Tenant in a Rented Flat: Do I Need Contents Insurance?

Cheap Home Insurance in Your Area

Quickly compare over 3 dozen UK insurance providers. Only one form to fill out.

Many tenants don't even think about buying contents insurance until either they or a friend suffer the loss of their possessions, perhaps due to fire or when their home is burgled or flooded. However renters aren't covered by the landlord's buildings insurance.

This comes as a surprise to many renters and is the reason that tenants should consider buying a contents insurance policy, which provides a level of financial protection in case of an unexpected, traumatic event like burglary, fire or flood.

According to the Association of British Insurers, around 7.5 million households do not have home insurance. Most of us don't even realize the value of our possessions, from clothes & shoes to electronics, jewelry, book, art and more—but typically we own tens of thousands of pounds worth of things.

What's Covered by Contents Insurance for Tenants?

Contents insurance typically covers the cost to repair or replace your possessions (i.e., the things you take with you when you move house) if they're lost or damaged due to fire, flood or burglary—three reasons why you should have contents insurance. Items may be insured up to a per-item limit, and you may need to declare items over this limit. Bicycles and high-value items (e.g., an engagement ring or expensive watch) may cost extra to insure.

Types of Items Typically Covered by Contents Insurance

- clothes

- shoes

- books

- furniture

- artwork

- kitchen items

- rugs & soft furnishings

- electronics

- jewelry

- luggage

You can buy policies with different excess (i.e., the amount you pay toward any claim before the insurer pays out) and limits (i.e., the maximum amount of cover). Policies differ from insurer to insurer and there are many features to look out for, such as "away from home" cover, outbuildings cover, bike cover, valuables limits, etc. Be sure to read your policy documents carefully, so you understand what you're buying.

How Much Contents Cover Do I Need?

The Association of British Insurers' (ABI) estimates that an average 3-bedroom family home contains £55,000 worth of possessions. If you live in a smaller flat, your contents may or may not be worth less—it all depends on what you own. Trying to figure out how much you should insure your home contents for can seem like a daunting process. Most contents insurers offer home contents calculators, which you can easily find through a Google search.

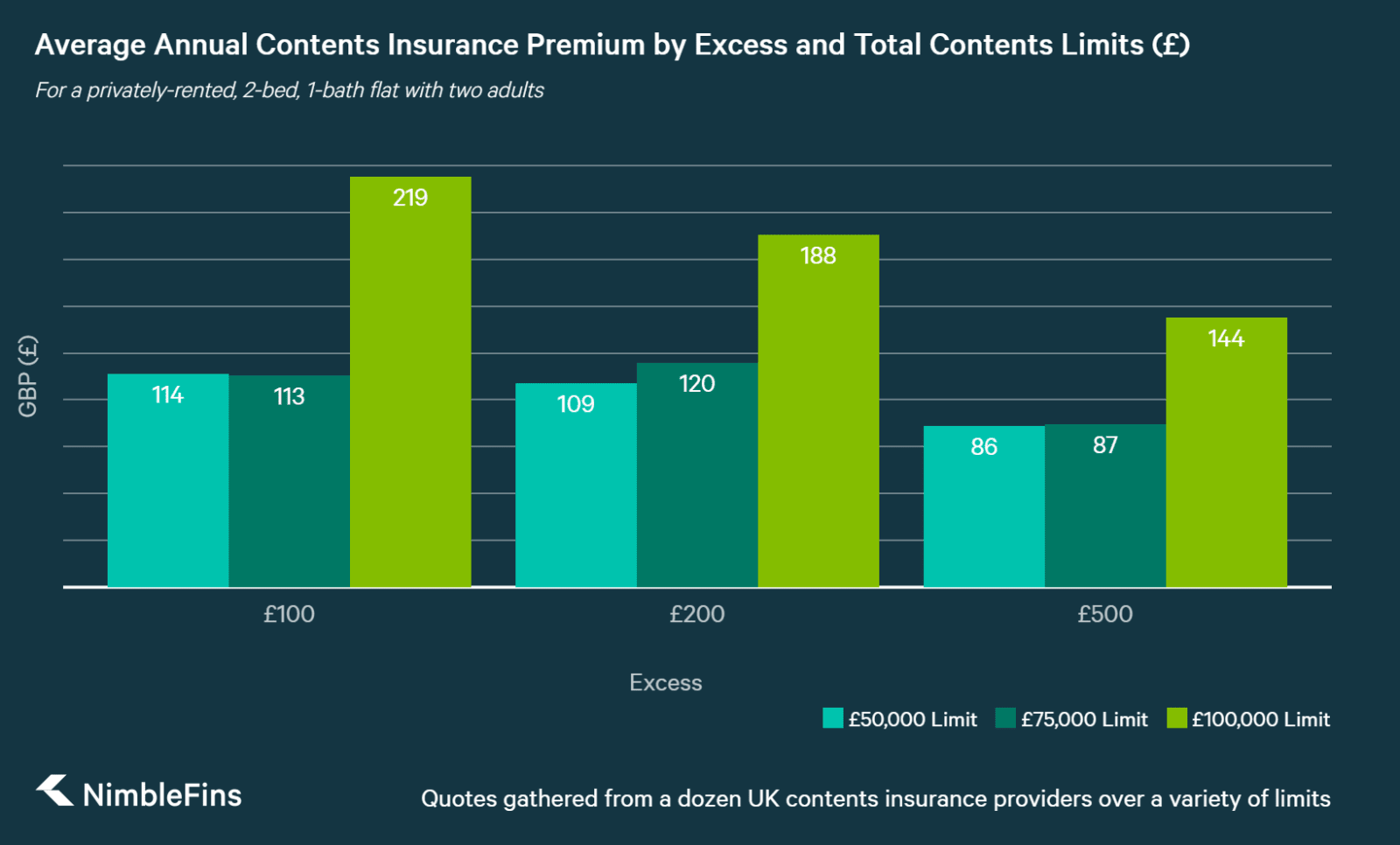

According to our research, the most common contents insurance coverage on offer is £50,000. Many policies offer variable limits, with the ability to increase coverage to £50,000 or even £100,000 or more. Some insurers offer unlimited contents cover, which might be worth looking into particularly if you live in a larger home. It is important to pay for sufficient coverage—if you under insure, you may not get the full value of claimed items.

Contents Cover for Tenants in Shared House

Even if you rent a room in a shared house, it can be a good idea to get contents insurance. Most policies will only cover in your room (not the shared areas) and require that your room is self contained—that is, you're able to the lock the door to your room when you're not there. Not all insurers offer shared housing contents insurance, but many do and there are specialist insurers providing the service also.

Average Contents Insurance Cost

You should expect to pay around £132-£138 a year for contents insurance in the UK, according to our analysis on the average cost of contents insurance. The ABI confirms this figure, with their most recent Home Insurance Premium Tracker finding that the average premium paid for contents insurance was £128 a year (~ £10.40 a month or £2.40 a week).

The cost will, of course, depend on the insurer, the level of cover, the excess, your location, etc. Prices can even vary considerably from one insurer to another. For example, we analyzed around 80 policies from a dozen UK insurers and found quotes for a privately-rented, 2-bed, 1-bath flat ranging from £57 to £392 per year.

Do I Need Contents Insurance if I Rent?

Just because you're renting, doesn't mean your possessions are any less valuable to you. Contents insurance can help alleviate the financial worry should you have to face a fire, flood or burglary. If you don't have it, take particular care if you go away on holiday or at certain times of the year, when burglary rates rise—for instance the months around Christmas are particularly prone to burglary when homes are filled with brand-new electronics, clothes, jewelry and other gifts.

If you're looking to buy contents insurance, start by reading through our research on the top picks for best home insurance companies.

FAQs

Each tenant in a shared house or flat should have their own renters insurance policy, unless they are part of the same family (e.g., spouses, children, partners). Consider the scenario where you share a policy that's in your name with your roommate, who claims on the policy—you would lose your no claims discount, even though you didn't make a claim. Also, you could have problems if your roommate moves out. And the benefit to having separate policies is that you can each establish your own insurance history, which can save you money in the long term.

Some landlords may insist that you have a renters contents insurance policy in place as part of your lease agreement. Landlords CAN require it as part of lease terms, though it's not mandated by law. And the landlord can always choose to rent to someone else who will take out cover as they'd like—so if there's a place you really like it might be worth stepping up.

Yes, a leak that causes water damage to your possessions would generally be covered by renters insurance. Your landlord's buildings insurance would take care of any damage to the building itself in case of a flood.

Renters do not need to pay for home insurance (which usually covers both buildings and contents), but they should consider taking out a contents only policy to protect their possessions in case of fire, theft or flood.

Cheap Home Insurance in Your Area

Quickly compare over 3 dozen UK insurance providers. Only one form to fill out.