AA Low Rate Card Review: Long-Term Low Rates, Great if You Sometimes Carry a Balance

AA Low Rate Card Review: Long-Term Low Rates, Great if You Sometimes Carry a Balance

Good for

- Keeping interest charges relatively low

Bad for

- Those looking for a low fee on balance transfers

- Individuals wanting a 0% promotional period on balance transfers

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Note: The AA Low Rate card is currently not available to new applications.

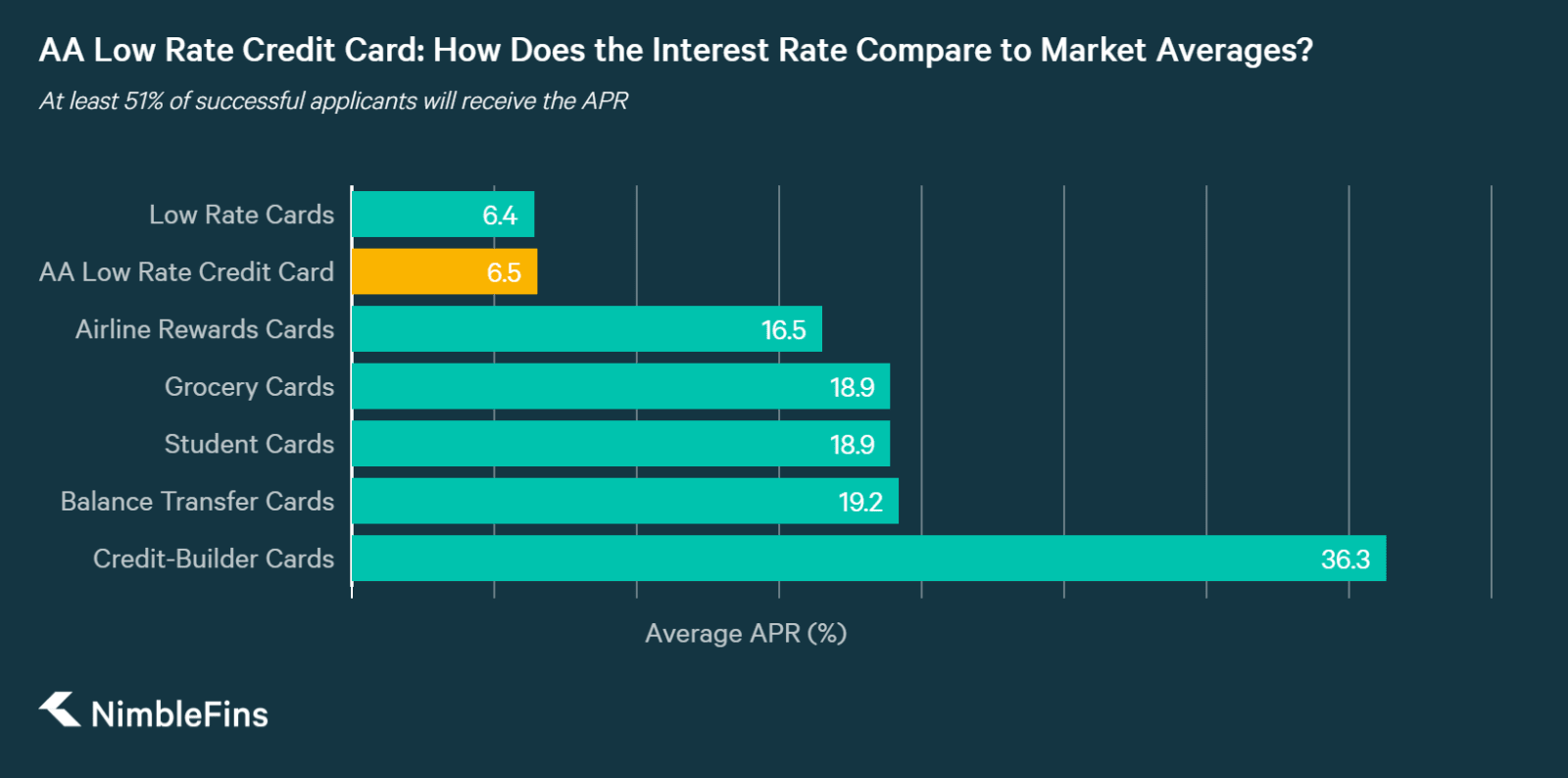

With its 6.5% APR, the AA Low Rate Credit Card can be a great option for those who may need to carry a balance—whether occasionally depending on circumstances or over an extended period of time. A key benefit of using a low rate card such as the AA card (vs. a 0% card) is that your low interest rate should hold steady over the long term—opposed to a 0% promotional purchases or balance transfer card, where your rate will eventually jump up to the stated rate of 18.9% or more when the promotional period ends (which can happen suddenly due to a late payment or surpassing the credit limit).

AA Low Rate Credit Card Review

The AA Low Rate Credit Card can be a reliable and steady tool in the wallets of those who be unable to pay off their credit card balance in full from time to time. With a low interest rate of 6.5% APR (variable) on purchases and balance transfers, the AA Low Rate card can help those managing their debt without paying excessive interest charges.

Low Rate Card vs. 0% Card: While you can certainly find competing credit cards in the market with a 0% APR promotional period, these no-interest cards are not without risk. A 0% promotional period will end at the end of the promotional period or can be brought to an abrupt and early end if you miss a payment or exceed your credit limit—in either case, your balances will start incurring interest at the stated rate of your card, which is likely to be 18.9% or more.

Anyone who from time to time is late on a payment or exceeds their credit limit may save money in the long run by using a low rate card instead of a 0% promotional card. These consumers may prefer to lock in a credit card that charges a reliable, lower-than-average interest rate, such as AA's 6.5% Low Rate card.

AA Low Rate Interest Rate: Not everyone will receive the representative 6.5% APR—but at least 51% of successful applicants will get this low rate. Other successful applicants may get 10.4% or 14.9% APR. Generally speaking, those with weaker credit histories will have to pay the higher interest rates.

Eligibility Check: AA can check your odds of being accepted before you apply (at which point a hard check is performed, leaving a mark on your credit record). The results of this free eligibility check are a guide only and not a guarantee, but it's certainly good to see if you're likely to be accepted before you apply. As part of this soft, pre-application check, you'll need to provide AA with details such as your employment status, estimated annual income, residential status, date of birth and address.

Balance Transfers: While you can transfer a balance to the AA Low Rate credit card, be aware that you'll pay a fee of 2.99% to do so. Transferred balances would then be subject to your stated interest rate (6.5%, 10.4% or 14.9%, as with purchases). There are certainly cheaper, promotional balance transfer offers in the market (e.g., up to 20 months of 0% interest for a 0% transfer fee)—but remember that these 0% promotional periods are at risk of ending early you are late on a payment or exceed the credit limit of your card. If you have a history of either of these, the AA balance transfer card could be a better deal for you with its low rate.

| AA Low Rate APR Comp | APR |

|---|---|

| AA Low Rate Credit Card | 6.5% |

| Market average low rate cards | 6.4% |

| Market average balance transfer cards | 19.2% |

Bottom Line: The AA Low Rate Credit Card can be a handy tool to help consumers lock in a low credit card rate over the long term, for times when they can't pay their full balance. With its representative 6.5% APR, the AA Low Rate card can make a good alternative to 0% cards especially for those who may occasionally make a late payment or exceed their credit limit (acts which could invalid a 0% promotional period on a 0% card).

AA Low Rate Card Benefits & Features

| AA Low Rate Credit Card Features | |

|---|---|

| Transaction Fees | Non-sterling transaction fees of 2.99% |

| Cash Withdrawal Fee | 2.99% handling fee, minimum of £3 per transaction |

| Balance Transfer Fee | 2.99% |

| Initial Credit Limit, minimum | £1,000 |

| Annual Fee | £0 |

| APR | 6.5% or 10.4% or 14.9% on purchases, cash withdrawals and balance transfers |

How does the AA Low Rate Card Compare to Other Credit Cards?

To better understand the value of the AA Low Rate Credit Card you need to look at it in the context of other available options. We compared this card to other cards so you can see which may be more suitable for you.

AA Low Rate Card vs Tesco Low Rate Credit Card

The Tesco Low Rate Credit Card is another good credit card for those wanting to lock in a low rate for the long term with a 5.9% APR. Tesco credit cards also act as rewards cards, earning Clubcard points when you spend at a rate of 1 point for every £4 spent (£4 minimum) in Tesco and 1 point for every £8 spent (£8 minimum) outside Tesco per transaction. Tesco Bank does not offer a pre-application eligibility check.

Quick Takeaway: While at 5.9% APR the Tesco rate is a bit lower than the AA 6.5% APR, those who prefer to see their odds of being accepted before they apply through an eligibility check may prefer the AA Low Rate card.