How to Understand your Credit Card Bill

Credit card bills can be confusing to understand, so we've created a guide to help you understand the various fees, interest charges, amounts due and dates you need to worry about. Learn about what's on your credit card bill, as well as best practices for managing your account to keep your credit score healthy.

In this article

- What's on a Credit Card Bill?

- Top Tips for Paying Your Credit Card Bill

- How do I contact my credit card company?

What's on My Credit Card Bill?

Your credit card bill will show your outstanding balance, new transactions made that month, any fees or charges incurred (e.g., foreign transaction fees), the minimum required payment, and the date your next payment is due. Here is a breakdown of what you might find on your bill:

Previous Balances

Any balances that you didn’t pay last month will show on your bill. This includes balances previously transferred (for instance if you have a balance transfer credit card), purchases and/or cash withdrawals made in previous months. You are charged interest on these carried-over balances.

New Purchases

All new purchases you’ve made during the month will be listed on your bill. Always look through this list to be sure you recognize each charge; if you don’t, you’ll need to call your credit card company.

Balance Transfers

If you have ever transferred a balance from a different credit card to your new credit card, this transferred balance will appear. Be aware that transferred balances may have different interest rates than your purchases. Also, there may be a one-time transfer fee on your new card in the month you moved the balance from one card to another.

Cash Withdrawals

Withdrawing cash from an ATM using your credit card is usually quite expensive. For starters, most cards start accruing interest charges immediately on cash withdrawals (unlike purchases, where you can get a grace period up to 56 days if you pay the full balance each month). In addition, credit cards typically charge a fee to get a cash advance. Unless you have one of the few travel cards that offers a grace period on foreign cash or doesn't charges fees on cash withdrawals, it's not usually economical to withdraw cash from a credit card.

Interest

Unless you pay off your balance in full every month, you will find interest charges on your statement. Interest will be charged on all balances that you carry over from the previous month. Interest rates may vary across different components of your balance: purchases, balance transfers, and cash withdrawals. Also, be aware that your interest rate may change (e.g., when an introductory 0% interest period comes to an end or the Bank of England raises rates).

For more information on what the APR means and how interest charges are calculated, read our article What is Credit Card APR? and our research on the average credit card interest rate. It is important to note that as of January 2026, the average credit card interest rate (APR) in the UK has reached 24.66%, the highest level in over 30 years. Understanding how these charges are applied to your bill is now more critical than ever for avoiding long-term debt.

Fees

Beyond interest charges and minimum payments, there are a number of fees you may see on your credit card statement. Some of these fees are:

Annual Fee/usage fee: Some cards charge an annual fee for using the card. This usage charge may be charged once a year or broken up into 12 monthly payments. Most cards in the UK charge no annual fee, but some of the best rewards credit cards charge fees ranging from £25 to £300 a year. A few cards charging annual fees will waive the fee the first year (e.g., Amex Preferred Rewards Gold card).

Transaction Fees: Depending on the terms of your card, you may be charged a transaction fee for balance transfers, cash withdrawals, or non-sterling transactions. Balance transfer fees usually range from 0% to 4.25%. As of January 2026, while short-term offers may still be fee-free, fees for the longest interest-free deals often reach 3.49% (offered by lenders like TSB, NatWest, and RBS) and can go as high as 4.24% for certain providers. Cash withdrawals and non-sterling transaction fees are typically around 3%, with a £3 minimum per transaction. (Some travel cards waive cash and/or non-sterling transaction fees entirely.) These transaction fees will be included in your monthly minimum payment due.

Default Charges: Cardholder error can result in further charges appearing on your monthly statement. Late payments, returned payments (e.g., a bounced cheque), and going over the credit limit will all incur default charges, typically around £12.

Paying Your Credit Card Bill

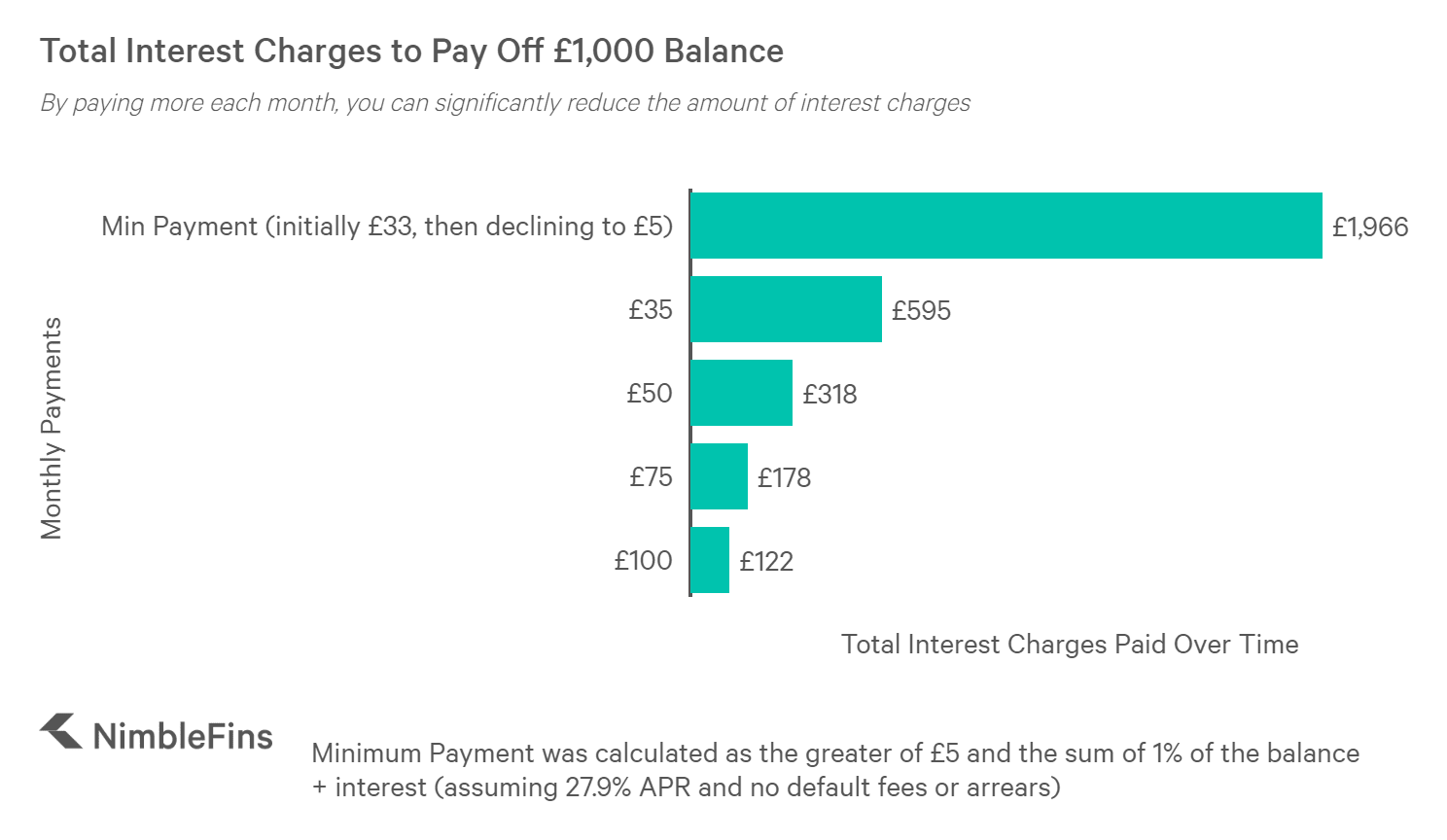

Always try to pay your credit card bill on time. Late payments will incur a charge and result in a mark on your credit history. At the very least, make your minimum payment. (If you cannot do this, call your credit card issuer to discuss.) Ideally, you will pay down your entire balance every month—this way you avoid all interest charges. Pay as much of the balance as you can, so the next month you will have a smaller interest charge to pay.

The chart below shows the difference between paying just the minimum amount due each month and paying a higher amount. As you can see, paying the minimum amount only is VERY expensive over time.

When Do I Pay my Credit Card Bill?

Each statement will have a payment date, which is the date by which the issuer must receive payment. If your payment arrives late (or not at all), you'll be charged a late payment fee and a notice may be sent to the credit agencies, affecting your credit score.

Some issuers let you change the payment date, a useful feature for those who want to coordinate their credit card payment with their pay day. Or for those who sometimes forget to pay on time, changing the payment date to coincide with other credit card or household bill due dates can help you remember to pay. While we like to think that paying online is quick, it may take a day or two for your payment to process, especially over the weekend or bank holidays. Be sure to send your payment a few days early as buffer. If you forget and send the payment last minute, call the card company to let them know the payment is on its way and you may avoid a late charge.

Minimum Credit Card Payment

The monthly payment is the minimum amount you must pay to your credit card each month, in order to avoid late fees and marks on your credit report. This minimum monthly payment will be much less than your total outstanding balance. The actual amount will vary by issuer, but at a minimum the calculation is generally:

Minimum Monthly Payment = 1% of the balance + interest charges + default charges + annual fees (whether charged once a year or monthly)

Some issuers may impose a further condition on the minimum payment. While some still use a low £5 floor, several major providers, including American Express and Virgin Money, now have a significantly higher minimum floor of £25 (or the full balance if it is less than £25). This is a crucial distinction for cardholders to keep in mind when managing their monthly cash flow. That said, a higher minimum payment is beneficial for consumers because it lowers the overall interest a cardholder pays back over time, if they're only paying the minimum amount each month.

What if I Pay My Credit Card Bill Late?

Late payments will incur a default fee/charge, typically around £12. This fee will be tacked onto your next bill, as part of your minimum monthly payment. A notice of the late payment may be sent to the credit card agencies and show as a mark on your credit report.

If you do sometimes forget to pay on time, there are a few strategies you can use to help. First, many cards offer text and email reminders for payment due dates; make sure these reminders are switched on. Second, set up a Direct Debit to take the minimum payment or even the full balance (if you have the funds in your current account) on the due date, which can be a good way to avoid late payments.

How are Payments Applied?

In the UK, payments are applied to the most expensive parts of your balance first. According to the terms of your card, there may be different interest rates for purchases, balances transfers, and cash withdrawals. If the highest interest rate is on cash withdrawals, for example, then any payment you make will first go to pay down any cash transactions.

Grace Period: How to Avoid Paying Interest

You can avoid paying any interest charges on new purchases IF you pay the full balance on time each and every month. Most cards offer a grace period from the date of purchase up until your next due date, which can last up to 56 days. During this grace period you are not charged interest on purchase balances, so long as they are paid off by the next statement date. You'll have had to pay in full the month before as well.

This grace period does not usually apply to cash withdrawals—cash advances start accumulating interest charges immediately on most credit cards, which is why withdrawing cash on a credit card is generally a bad idea. Some travel cards make an exception and offer a grace period on foreign cash withdrawals, like the Barclaycard Rewards Travel Card.

What if I go Over the Credit Limit?

Like late payments, going over your credit limit will result in a default fee on your next statement, usually around £12. This fee will be added onto your next monthly minimum payment. Like late payments, notice may be sent to the credit agencies that you've exceeded the credit limit, and a mark may appear on your credit history—avoid these if you're trying to improve your credit score.

What if you Don’t Recognize a Charge?

It is important to look through the new purchases on your card, to spot potential fraudulent charges. If you don’t recognize a charge you should contact your credit card issuer immediately. However, be aware that sometimes retailers show up under a different name on your credit card statement (e.g., if the retailer is part of a larger organization). You may want to perform an Internet search to see if any unrecognizable names on your statement are related to places you’ve shopped at recently.

Contacting Your Credit Card Company

Here is a list of phone numbers and payment websites for the largest credit card issuers in the UK.

| Issuer | Billing Phone Number | Online Login & Billing |

|---|---|---|

| American Express | 0800 917 8047 | American Express customer service contact |

| Asda Money | 0371 704 3369 | Asda Money customer service contact |

| Aqua | 0333 220 2691 | Aqua customer service contact |

| Barclaycard | 0800 151 0900 | Barclaycard customer service contact |

| Creation | 0371 376 9214 | Creation customer service contact |

| Halifax | 0345 944 4555 | Halifax customer service contact |

| Lloyds | 0345 300 0000 | Lloyds customer service contact |

| Marbles | 0333 220 2692 | Marbles customer service contact |

| MBNA | 03456 062 062 | MBNA customer service contact |

| Sainsbury’s | 08085 40 50 60 | Sainsbury’s customer service contact |

| Santander | 0800 9 123 123 | Santander customer service contact |

| Tesco Bank | 0345 300 4278 | Tesco Finance customer service contact |