RBS Student Credit Card

Good for

- Students needing their first credit card

- Establishing your credit history

- Getting a relatively low rate for a starter card

- Being accepted for a credit card with no income

- Having branches nearby

- International students

Bad for

- Opening a new credit card without an associated bank account

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Update: RBS no longer offers a student credit card. This review is left up for historical purposes.

The RBS Student Credit Card can be a great option for students in the UK, including international students, so long as they also have a RBS student bank account. Learn about the features to help you decide if it's right for you.

RBS Student Credit Card Review

Like other "student" credit cards, RBS will consider applicants without income or an established credit history and can be a great way to work on building your credit history before you leave school. To get the most out of the card, be sure to pay on time each month and always stay under your credit limit or you risk harming your credit score—plus paying late or going over your limit will cost you £12 each time.

The mobile app has some great features not found on other cards, such as:

- Ability to lock/unlock your credit card

- Analyse your spending

- Order a replacement card

- Notify RBS of travel plans to help avoid problems

- Make payments

- Go paperless

Since the account is targeted at students who may not have had credit before or a job. Basic requirements to be accepted are being a UK resident, 17 years of age and a student. Proof that you are a student is required.

The RBS Student Credit Card is a solid option for students looking to open their first bank account and associated credit card in part because the 18.9% APR (variable) purchase interest rate is lower than you'll find on other credit-builder cards. Applicants don't need proof of income, so students needn't worry about this requirement of so many other credit cards.

What interest rate will you get? At least 51% of cardholders will receive the 18.9% rate; the rest may pay a higher interest rate on their purchases. Interest on cash is nearly 10 percentage points higher, at 27.9% APR (variable).

Ways to use the RBS Student Card

- Apple Pay

- Google Pay

- Paym (using a telephone number and the RBS mobile banking app) for sending money

- Contactless up to £30

Ways to make payments to your card

- Direct Debit (set up to pay the minimum amount, a fixed amount or your full credit balance every month)

- Via the mobile app

- Digital banking

RBS Student Credit Card Benefits & Features

| RBS Student Credit Card Features | |

|---|---|

| Initial Credit Limit | Up to £500 |

| Transaction Fees |

|

| Eligibility checker | To see your odds of being accepted |

| Other Features | Mobile Banking, Direct Debits, Standing Orders |

| Annual Fee | £0 |

| APR (variable) |

|

Who Can Apply?

Like other high-street bank student credit cards, you can only open an RBS Student Credit Card along with an RBS Student bank account. To open a student bank account, you must have a confirmed place to study and:

- Be at least 18 years old

- Have a RBS Student bank account

- Be a UK resident

Students will be considered by RBS for the student account if they are either in:

- a full-time undergraduate course that lasts at least 2 years

- or a full-time post-graduate course

- or training as a nurse at a UK university or college of higher education.

As proof of student status, RBS requests a 16-digit UCAS Status Code, which will have been emailed to you by UCAS.

Student Bank Accounts for International Students

It is possible for international students coming from abroad to be accepted for the RBS student account and credit card. But you must have a UK residence established before doing do. The only feature not available to international students is the Student Arranged Overdraft, so international students need to keep their bank account in the black.

International students may prove their students status in the following ways:

| Proof of Student Status | Requirements |

|---|---|

| UCAS Letter | On headed paper |

| Including the UCAS application number | |

| Address must match that on the RBS application form | |

| NMAS Letter of Acceptance | On headed paper |

| Including the NMAS application number | |

| Address must match that on the RBS application form | |

| Student Loan Company/LEA/SAAS Award Letter | On headed paper |

| Address must match that on the RBS application form | |

| Uni/College Letter of Acceptance/Enrolment Offer/ Enrolment Certificate | On headed paper |

| Addressed to the Bank or to you at your application address | |

| Original letter, an email or an internet print | |

| Letter must confirm you are onto the course and match the address on the application form | |

| Letter must be issued by a Government/LEA/SAAS funded University/College | |

| Letters from a language schools are not acceptable | |

| The course must still have six months left to run, unless it’s an English course ahead of another higher ed/uni course |

What is a Grace Period?

A "grace period" refers to an interest-free period on a credit card. You'll get the grace period on new purchases if and when you pay the full balance by the next due date. For instance, if you spend £100 using your credit card and pay back the full £100 before the next due date, you won't be charged any interest (even though you technically borrowed money from the time of the purchase until you repaid the full balance.) By paying the full balance on time every cycle, you will never pay interest charges on your credit card.

All UK credit cards offer a grace period on purchases. Grace periods on other transactions such as cash withdrawals and balance transfers are unusual.

What is the Minimum Payment?

Each month, you're required to pay at least a minimum portion of the amounts owed on your card. Assuming you stay within the credit limit, the minimum amount will be calculated as 1% of your outstanding balance + and Default Charges + any interest due. Or, if your balance falls below £5, RBS asks you to pay the full outstanding amount to clear the account.

Paying ONLY the minimum amount due can be very costly, however, as interest charges accumulate on amounts carried over from month to month. By paying back as much as possible each month, interest charges can be limited—paying the full balance on time each month means no interest charges at all.

Credit Building

By using the RBS Student credit card responsibly, students can work to establish a healthy credit history. Most important are to always stay within your credit limit and make on-time payments (of at least the minimum monthly payment).

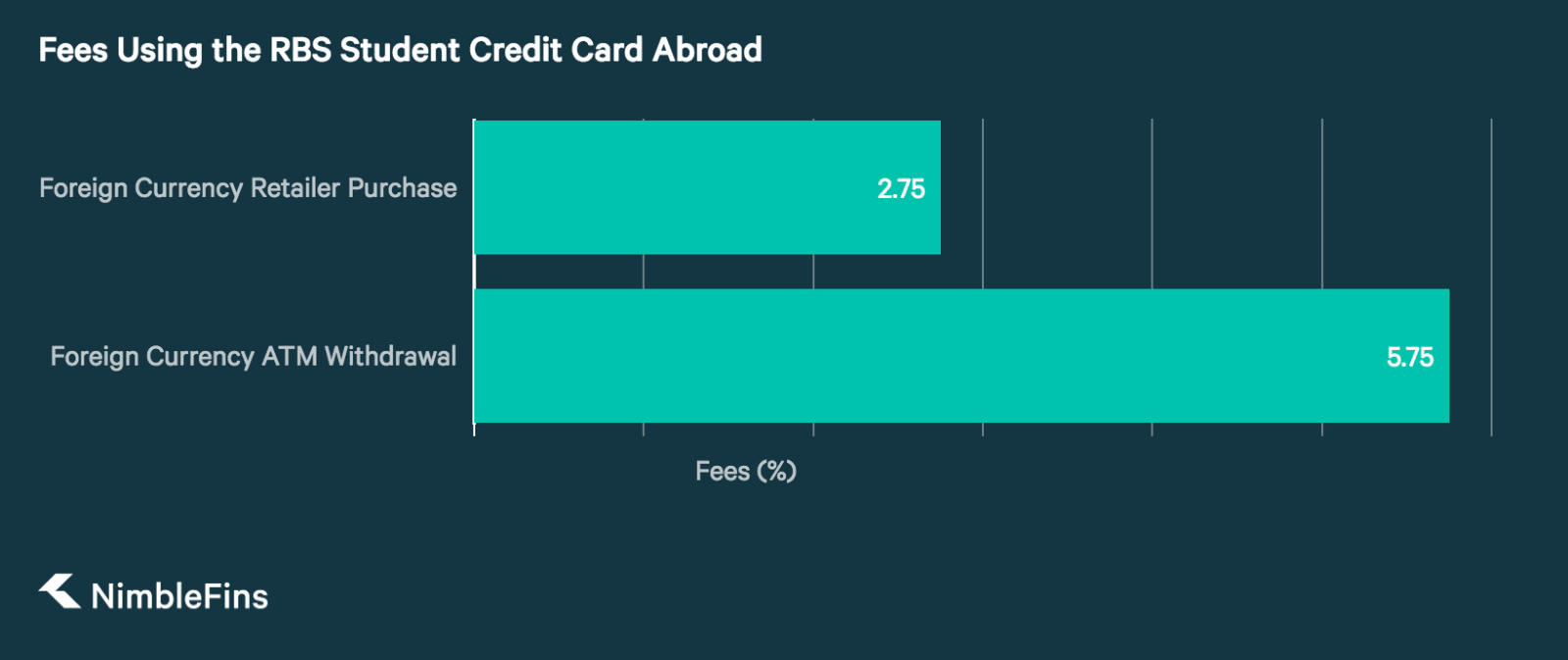

Using RBS Student Credit Card Abroad

Anyone planning to use their student credit card abroad should be aware of the potential fees and charges, as they can really add up. All non-sterling transactions incur a 2.7% fee, plus cash withdrawals from an ATM cost an additional 3% of the transaction. Furthermore, cash withdrawals are charged interest immediately and at a higher rate than you pay on purchases. Here are the fees for using the RBS Student Credit Card overseas. Withdrawing cash is always expensive on a credit card, and even more so from abroad—if you must withdraw cash using the credit card, try to pay back any balances ASAP to limit interest charges.

| Type of Transaction | Example | Fee | Minimum Fee |

|---|---|---|---|

| Credit Card Purchases | Paying for a meal in a restaurant | 2.75% | n/a |

| Cash Withdrawal | Getting foreign cash from an ATM | 3% + 2.75% = 5.75% | n/a |

Should I Pay in Pounds Abroad, to Avoid the Foreign Transaction Charge?

Usually, it's more economical to pay in the local currency when you're abroad, because if you choose to pay in pounds then the retailer picks the currency exchange rate—which can be suboptimal, and they may charge you for doing so. The other option is to pay in the local currency and incur a 2.75% foreign transaction fee. You can learn more about cards that do not charge foreign transaction fees in our guide on Travel Credit Cards.