The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Travel insurance for over 70s - best cheap travel insurance including for pre-existing conditions

Travel Insurance

for Over 70s

with Just Travel Cover.

Get Quotes

- /5 stars on Reviews.co.uk

- 1,000,000+ passengers insured over 20 years

- Access to multiple insurance companies

- Approved specialist medical travel insurance

Over 70 years old and need travel insurance, but have questions or not sure where to get quotes? It can be confusing, with fewer providers offering cover, limits on annual policies and needing to declare pre-existing conditions. Below we'll try to explain what you need to know to find the cover right for you.

If you're after quotes, you can click the blue button above to get started. Or if you don't have any pre-existing medical conditions, you might find a cheaper price from our partnership with QuoteZone (get quotes here).

- Travel insurance for over 70s

- Best travel insurance for over 70s

- Cheap travel insurance for over 70s

- Travel insurance for over 70s with pre-existing conditions

- Travel insurance for over 60s

Travel insurance for over 70s

Travel insurance for over 70s is extremely important, in part due to the higher risk of a serious medical event for older travellers. Having a heart attack, stroke or simply a fall while abroad could lead to significant medical bills. And travel insurance can essentially cover these costs.

In addition there may be a higher risk of needing to cancel a trip due to an unexpected event like illness of you or a close family member, which could necessitate a claim on the cancellation portion of a travel insurance policy.

But travel insurance changes a bit once you hit 70 years old, with higher costs, fewer policies on offer and more restrictions. Below, we'll do our best to explain what to be aware of, what you mind find and how to pick the best policy for you. Any questions? Please let us know in the comments section at the end of this article.

Higher travel insurance costs for over 70s

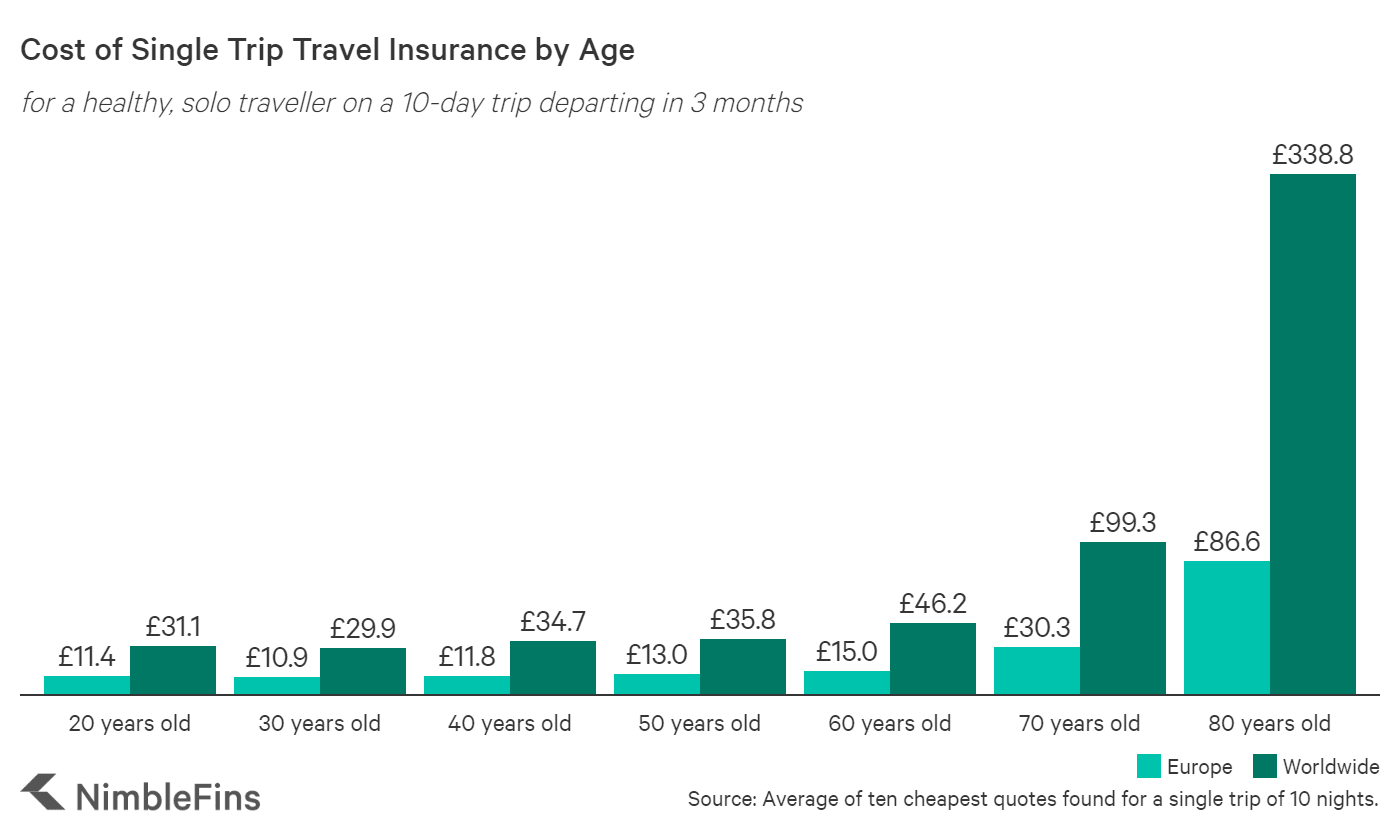

For these reasons, the cost of travel insurance for over 70s is a lot higher than for younger travellers. In fact, by the time you're 70 or 80 years old, you'll notice that prices really jump up.

We've run a lot of pricing tests and found that a healthy 80 year old would pay around 10X as much as a 30 year old—add in some pre-existing conditions and prices will be even higher. This premium for older policyholders has risen since the onset of the pandemic—80 year olds used to be 7X more expensive to insure than 30 year olds. But perhaps this is not surprising considering the potentially high health costs associated with a Covid-related hospital admission.

Prices below reflect the average of the 10 cheapest plans found for different ages, for cover rated at least 3 out of 5 stars.

Less access to annual policies

In addition to price, we should point out another difference in over 70s travel insurance compared to cover for younger people: you may find it harder to get annual trip cover. That is, you will find that some insurers will only offer you single trip cover.

In part this is due to the reasons related to what we discussed above, namely that there's a higher risk of policyholders developing a serious medical condition over the course of a year. As a result an insurer may be reluctant to offer a policy that could cover unlimited trips, with some up to a year from the date of purchase. To limit their risks, they may only sell you cover for single trips.

Note: One of the many reasons we like Just Travel and have a relationship with them is that they DO offer annual policies to older travellers—and even offer annual policies to those in their 80s! Note: if you select single trip cover they'll show you the providers offering single trip cover, obviously, but they'll also show the premium for upgrading to an annual policy. We really like this feature so you can view and compare prices for single trip and annual cover at the same time. Get quotes here.

Shorter Trip Lengths for over 70s

Also, be aware that some insurers will limit the duration of trips for older travellers; that is, the maximum trip length may be shorter for over 70s than it is for younger travellers. For example, the Post Office policy wording says this about maximum trip duration for single trip cover:

- 365 days for persons aged up to and including age 70

- 90 days for persons aged between 71 and 75

- 31 days for persons aged between 76 and 85

Where ages refer to the age upon the date of purchase of the policy.

Needing to buy in person or over phone (not online)

Insurance providers might also limit the ways you can purchase a policy, if you're over 70. For example, sticking with the Post Office, they say:

If you are aged 75 cover is only available to purchase from the Post Office website or the Customer Care team.

That is, if you're over 75 years old you can't buy a policy in person at the Post Office.

Limited add-on features

It's also common to find limitations on winter sports cover for over 70s as well, e.g. a company might not offer it based on your age.

Best travel insurance for over 70s

Travel Insurance

for Over 70s

with Just Travel Cover.

Get Quotes

- /5 stars on Reviews.co.uk

- 1,000,000+ passengers insured over 20 years

- Access to multiple insurance companies

- Approved specialist medical travel insurance

While there is no one 'best' policy for everyone, since people have different needs and budgets, we find it really helpful to compare certain features to help identify some of the best providers in the marketplace. Below, we rank companies offering travel insurance for medical conditions like high blood pressure, cancer, asthma, heart attack and more (since many over 70s have some kind of pre-existing medical condition).

| Rank | Pre-existing Travel Insurance Provider | Terminal prognosis cover | Medical equipment cover | Cover for trips more than 12 months out | Medical screening | Customer Rating | Customer Reviews |

|---|---|---|---|---|---|---|---|

| 1 | Justtravelcover.com | yes | up to £2,500 | yes | Verisk | 4.7 | Customer reviews |

| 2 | AllClear Insurance Services Ltd | yes | up to £2,500 | no | Verisk | 4.8 | Customer reviews |

| 3 | Free Spirit | yes | up to £2,000 | no | Verisk | 4.7 | Customer reviews |

| 4 | goodtogoinsurance.com | yes | up to £2,500 | no | Verisk | 4.7 | Customer reviews |

| 5 | Insurancewith | yes | up to £5,000 | no | Protectif | 4.8 | Customer reviews |

| 6 | Media Travel Insurance Services Ltd | yes | up to £3,000 | yes | Verisk | ||

| 7 | Our Travel | yes | yes | yes | Verisk | ||

| 8 | Staysure | yes | no | yes | Verisk | 4.7 | Customer reviews |

| 9 | www.payingtoomuch.com | no | up to £2,500 | yes | Verisk | 4.9 | Customer reviews |

| 10 | able2travel | no | up to £1,000 | no | Verisk | 4.7 | Customer reviews |

| 11 | direct-travel.co.uk | no | no | yes | Verisk | 4.6 | Customer reviews |

| 12 | Holiday Extras Cover Limited | no | up to £3,000 | yes | Verisk | 4.3 | Customer reviews |

| 13 | Insure & Go Insurance Services Ltd | yes | no | no | Verisk | 4.8 | Customer reviews |

| 14 | InsureCancer | yes | up to £1,000 | no | Verisk | ||

| 15 | Royton Insurance Services | yes | no | yes | Verisk | ||

| 16 | Travel Insurance 4 Medical | yes | no | no | Verisk | 4.8 | Customer reviews |

| 17 | www.insurefortravelhealth.co.uk | yes | no | yes | Verisk | ||

| 18 | Andrew Yule Limited | yes | no | no | Verisk | ||

| 19 | Freedom Insurance Services Limited | no | no | no | Verisk | 4.9 | Customer reviews |

| 20 | G J Sladdin & Co Ltd | no | no | yes | Verisk | ||

| 21 | Rothwell & Towler Limited | yes | no | no | Verisk | 3.1 | Customer reviews |

| 22 | Thomas Carroll (Brokers) Ltd | no | no | no | Verisk | 4.8 | Customer reviews |

| 23 | Worldwide Travel Insurance Services Ltd | no | no | no | Verisk | 4.8 | Customer reviews |

| 24 | Brunel Insurance Brokers Limited | no | no | no | Medical screening in-house | 4.3 | Customer reviews |

| 25 | Global Travel Insurance Services Ltd | no | no | no | Medical screening in-house | 3.3 | Customer reviews |

| 26 | OK To Travel Ltd | no | no | no | Verisk | 4.5 | Customer reviews |

| 27 | Saga Services Limited | no | no | no | Verisk |

Cheap travel insurance for over 70s

It can take some extra research to find a cheap travel insurance policy if you're over 70, but the work is well worth it—especially if you're being quoted high premiums due to age or health conditions. Here we have some tips on how to save money when buying an over 70 policy, as well as some research on the cheapest travel insurance providers for over 70s.

How to save money on travel insurance for over 70s

There are a few ways to try to lower the cost of travel insurance for older travellers:

- Cancellation: If you're really struggling with the premiums you're being offered and primarily are worried about getting emergency medical cover while abroad, consider how much cancellation cover you really need. Getting a policy with less cancellation coverage can lower your premium. This can be an effective strategy because there are many 'cheap' policies on the market that have low cancellation cover, so they'll be cheaper, but still offer millions of pounds worth of medical cover.

- Excess: Some travel insurance policies give you some control over the excess you'll pay in case of a claim. If you opt for a larger excess (meaning you'll pay a higher portion of any problems), this should lower your premium. Just make sure you're able to pay the excess should you need to.

- Buy single trip not annual cover: If an insurer will sell you an annual (multitrip) policy, it's bound to cost a lot more than a single trip policy. Compare these costs carefully, taking into consideration how many trips you actually plan to take in the coming year. While you might have previously relied on annual cover when you were a bit younger, as you head into your 70s or beyond, you might find it more economical to purchase single trip cover.

- Buy a separate policy from your partner: If you're travelling and buying travel insurance with a partner, take stock of your pre-existing conditions. If one of you has serious pre-existing conditions that spike the cost of travel insurance, you might find that it's cheaper to buy individual policies. This may come with some inconveniences like admin on two separate policies, but it might be worth it.

- Compare policies: For this age bracket it's especially important to compare prices before buying. We can help with that. If you don't have any pre-existing medical conditions to declare, our sample traveller got the cheapest rates via our partnership with QuoteZone (get quotes here); someone with pre-existing medical conditions might prefer going to a specialist like our partner Just Travel who work with many providers and have policies tailored for this age bracket (get quotes here).

Cheapest travel insurance for over 70s

According to our research of dozens of policies from our partners, we found the following five companies offered the cheapest cover to our sample over 70s traveller:

| Cheapest over 70s travel insurance for a one-week trip to Europe | Get quotes | |

|---|---|---|

| Puffin | £28 | Compare quotes |

| Avion | £32 | Compare quotes |

| Unity Travel (AIG) | £33 | Compare quotes |

| insure for | £35 | Compare quotes |

| Leisure Guard Travel | £39 | Compare quotes |

Note, your quotes will certainly vary, and the cheapest provider for you might differ than for our sample 75 year old; our sample traveller did not have any pre-existing conditions. If you have those, you may pay more, all else equal.

Travel insurance for over 70s with pre-existing conditions

In the past 12 months, have your or another traveller been prescribed medication or received treatment (including surgery, tests or investigations)?

In the last 5 years, has any traveller taken and/or been prescribed medication or received treatment (including surgery, tests or investigations) for any cardiovascular or respiratory condition, or cancer, diabetes, epilepsy or stroke?

If you have pre-existing medical conditions, you most certainly need to declare them to your travel insurance provider. A lot of people over 70 years old have something in their medical history to declare, so the travel insurance companies are pretty adept at taking this information. In fact, most of them have online medical screening so you can often get a policy without speaking to someone. (This might not be the case for certain ages or conditions.) While a few travel insurance companies do their own medical screening in house, most screen with the help a medical screening company. The big one is Verisk—this company is used by the majority of travel insurance providers. Another one is Protectif.

Because of this, if you're struggling getting cover (at a reasonable rate) from one insurance provider, you may also struggle to get cover from another insurer using the same medical screening company. Just something to keep and mind and check if needed. You can see how a travel insurance company carries out its medical screening in the list of best over 70s travel insurance companies above.

Important note: If your heath changes AFTER you buy a policy, you'll still need to notify your travel insurance provider. And they may increase your premium as a result for covering a different or more severe condition (even if you've already paid in full). But you must do this or else your policy could be voided.

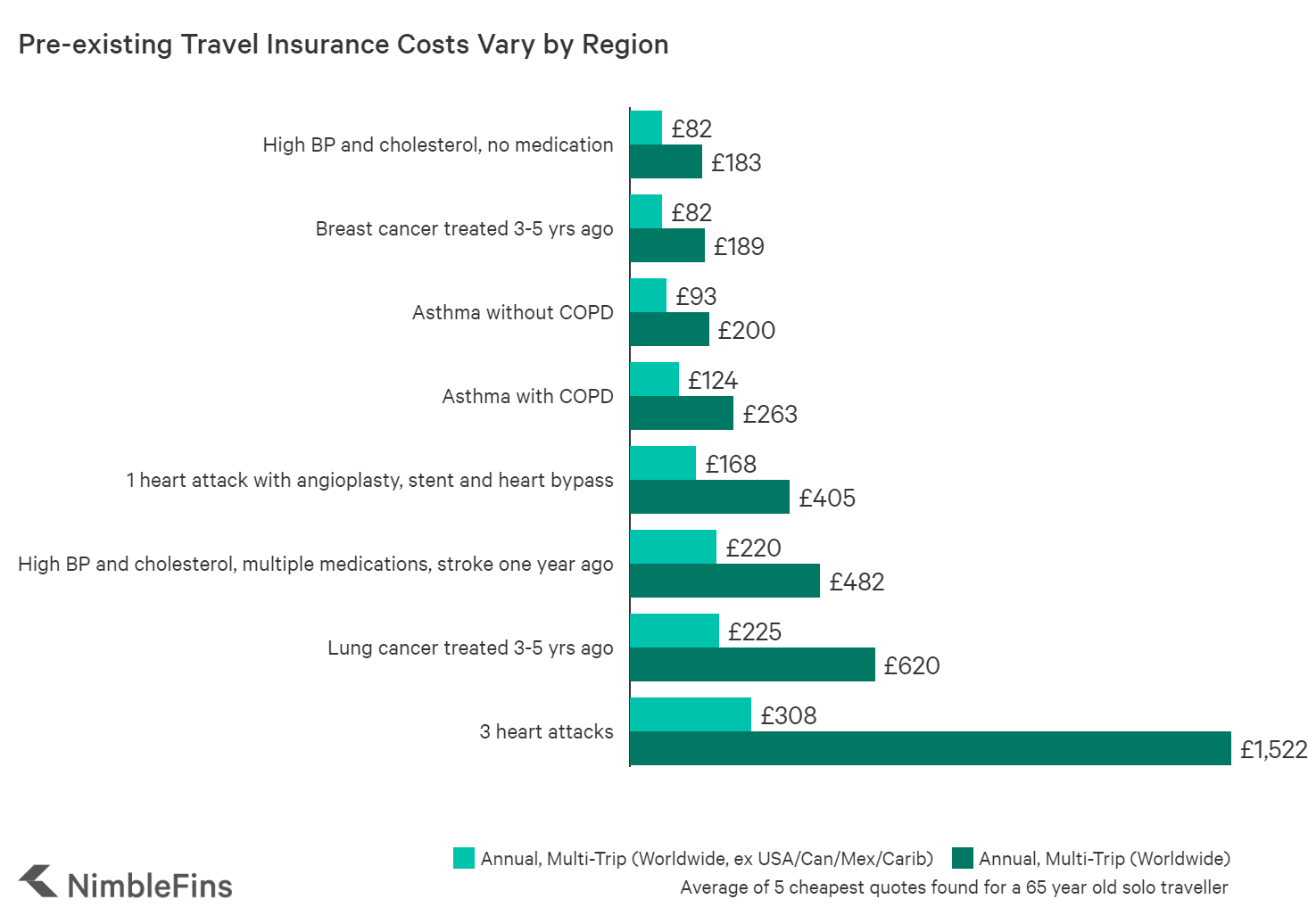

Below, we show some sample prices for travel insurance with different medical conditions, from high blood pressure and other heart issues to cancer and asthma. Your prices will certainly vary, but you can see how insurers take these conditions into account and price accordingly.

Is high blood pressure a pre-existing medical condition for travel insurance?

Yes, high blood pressure must be declared as a pre-existing condition for travel insurance. When making the declaration, you will be asked a few questions such as:

- if you're on any medication and, if so, how many medications you're on

- if your medications have changed in the past 6 months

- if you are or were a smoker in the past—if you've given up, how long ago you quit

- if you're on cholesterol medication

- if you have raised cholesterol levels

Do I need to declare arthritis on travel insurance?

Yes, you need to declare if you have arthritis to your travel insurance provider. You'll need to tell them what type of arthritis you have, e.g. inflammatory arthritis, osteoarthritis, psoriatic arthritis, reactive arthritis, rheumatoid arthritis, septic arthritis, etc.

Also, they might ask a number of questions, including but not limited to:

- which parts of your body are affected

- whether you've had joint replacement or joint resurfacing

- how many medications you're on

- if you're awaiting any joint replacement or joint resurfacing surgery

- if your joint replacement has ever dislocated

- how many unplanned hospital admissions you've had for this in the past few years

- etc

Do I have to declare diabetes on travel insurance?

Yes, you need to declare diabetes to your travel insurance provider as a pre-existing medical condition. First, you'll be asked to name the type of diabetes you have, such as diabetes type 1, diabetes type 2, pre-diabetes, sugar diabetes, diabetes insipidus, etc.

You may be asked to confirm:

- if you're over 16

- if you take insulin

- how many unplanned hospital admissions you've had in the past few years

- if you have or have had a wide range of other conditions, including amputation, angina, heart attack, kidney impairment, leg or foot ulcers, nerve damage, peripheral vascular disease, retinal eye damage, stroke, and possibly more

And depending on how you answer those questions, you may be asked for further information regarding your condition and treatments.

How far back to pre-existing conditions go?

It depends. Firstly, different travel insurance companies might have different rules regarding how far back they go for pre-existing conditions.

Secondly, any individual travel insurance company will likely look back for varying amounts of time, depending on the condition and situation. For example, Admiral might look back only 2 years, or they may look back indefinitely. Here's what they say in their policy wording:

Pre-existing medical conditions

- Any medical condition in the past 2 years, for which you were prescribed medication, received treatment or had a consultation with a doctor or hospital specialist

- If you’ve ever been diagnosed with or treated for any heart or respiratory condition, any circulatory condition (problems with blood flow, including strokes, high blood pressure and cholesterol), any liver condition or any cancerous condition

- If you are currently on a waiting list for tests, investigations, awaiting results, diagnosis or treatment

- If you have been diagnosed with a terminal condition

- If you have ever been diagnosed with or treated for any psychological conditions such as stress, anxiety, depression or psychiatric conditions such as eating disorders, drug or alcohol abuse or mental instability

As you can see from the above, how far back a travel insurance company goes is really variable.

Does taking statins affect travel insurance?

Yes, you will need to declare that you take statins to your insurer as a pre-existing condition. This falls under the 'high cholesterol' condition when you're going through the medical assessment. And you'll be asked questions like:

- if you take medication (e.g. statins)

- how many medications you take

- if your medications have changed in the past 6 months

- if you smoke or used to smoke

- etc.

The reason they ask if your medications have changed recently is that this could indicate a deteriorating help condition; also, your body could still be adjusting to a new medication or dosage, increasing the risk of needing a doctor visit while away.

Travel insurance for over 60s

Over 60s travel insurance has some limitations, but is broadly easier to get and cheaper than travel insurance for over 70s.

Some travel insurance providers won't offer cover to those over 65, or at least not annual policies. In that case, you may need to buy a single trip policy or look for another insurance provider.

In terms of price, you might need to pay a bit more than you did in your 50s, but the increase shouldn't be alarming, if there even is a price rise. As you can see in the chart below, it's really once you're in your later 70s, 80s and 90s that prices skyrocket.

Finally, you may like to read our related articles on worldwide travel insurance if you're doing a big trip or family travel insurance if you're taking any grandchildren along!