The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Are Credit Card Companies Targeting Those Struggling with Debt?

When paid off in full every month, credit cards can be a useful addition to a consumer's wallet. Credit cards can be used to earn rewards on spending or simply for the convenience and security of paying for purchases without the need to carry a lot of cash. For those struggling with debt, however, credit cards can make a difficult situation worse.

According to research from Citizens Advice, credit card companies are granting unsolicited higher credit limits to those already struggling with debt. This practice is problematic because it potentially increases the debt burden of those already suffering from problem debt. Following their research, Citizens Advice has called for a number of measures to be implemented by the Financial Conduct Authority (FCA), lenders and the government to help people avoid falling into a debt trap.

Citizens Advice Stuck In Debt - Results

Citizens Advice recently conducted a study called Stuck in Debt, which concluded that 18% of people who have a credit card and are already struggling with debt were granted a higher credit limit in the past year—without them asking for it. Of credit-card carrying individuals who are not struggling with debt, only 12% received an unsolicited credit limit increase. Due to these differences between those struggling with debt and those not, the concern is that credit card companies are specifically targeting those in financial difficulty.

While this study highlights historical trends, credit card debt remains a significant burden today; as of 2025, the average credit card debt per UK household reached £2,601.

Sometimes a Credit Limit Increase is Good

It is important to keep in mind one valid reason why those in a weaker financial position may receive credit limit increases more often – by starting off with very low limits and low credit scores they have more room to improve. Those struggling with their debt will naturally have weaker credit scores and, as a result, tend to receive small credit limits initially from a new credit card. Some credit-builder cards, for example, initially offer only £150 - £250 of credit to start.

As cardholders demonstrate financial responsibility by paying on time and staying under their credit limit, a card company may raise the credit limit on the account. So in a sense it seems realistic that credit card companies would raise limits more frequently for those with less than ideal financial situations – these cardholders can show the most change in their ability to handle debt.

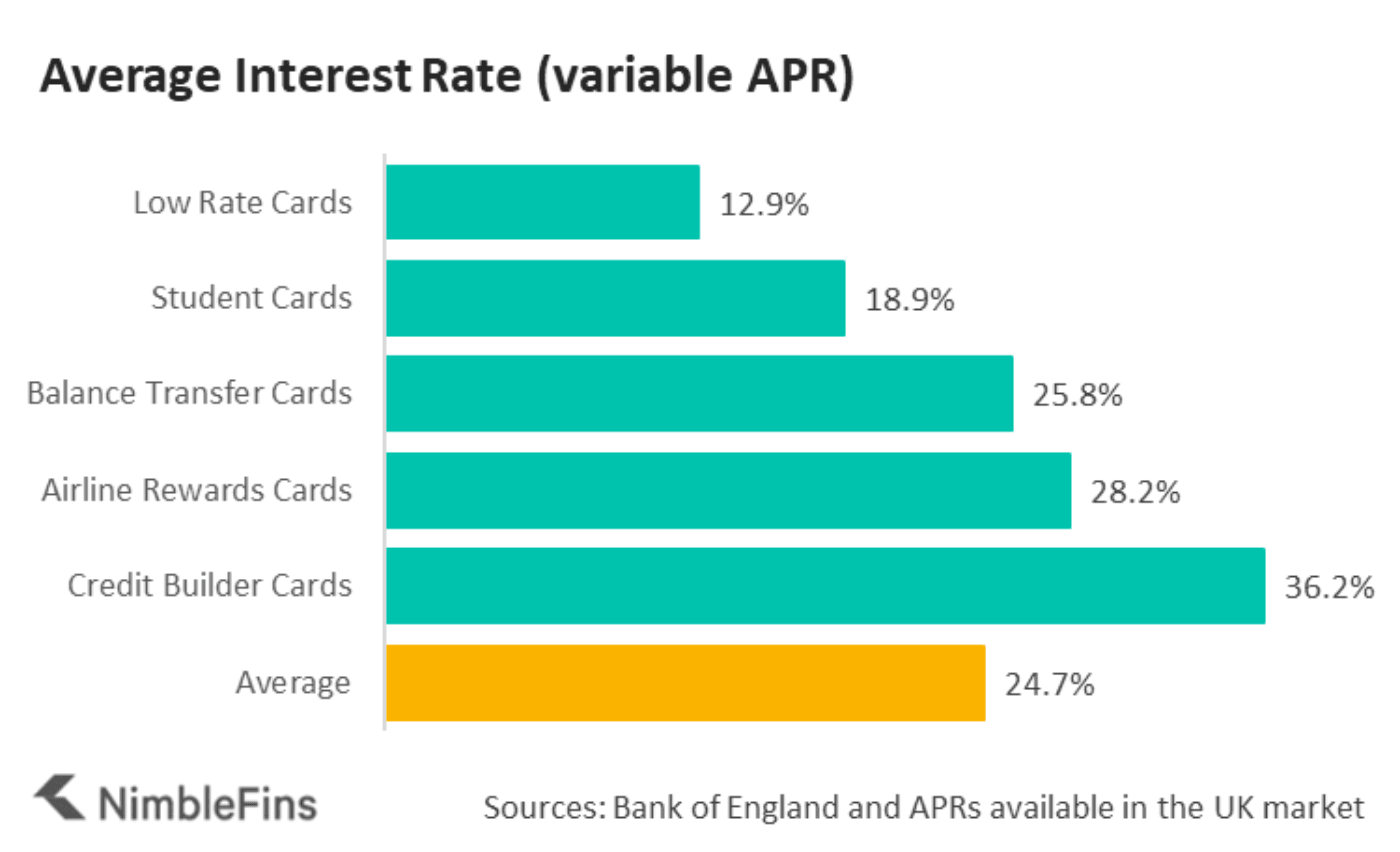

For many people, receiving a credit limit increase can be a good thing. Besides the fact that a higher limit can enable you to conveniently pay for more day-to-day expenses, a credit limit increase may improve your credit history. And a higher credit score generally means access to a wider range of credit cards, in particular cards that charge lower average interest rates and may even offer rewards on spending. As you can see in the following chart, those with poor credit can expect to pay interest rates over 2X higher than those with good credit.

When is a Credit Limit Increase Bad?

On the other hand, a credit limit increase can be a big problem for those who both use this increase (that is, take on more debt) and already have trouble paying back other pre-existing debt. This is particularly risky given the current scale of borrowing; as of 2025, the average UK household consumer debt (excluding mortgages and student loans) reached £8,304, rising to £18,392 when including all types of unsecured debt.

Anyone struggling with their existing debt is generally working to reduce outstanding debt—by providing higher limits, credit card companies may be enabling individuals take on more debt. It's like handing a luscious chocolate cake to someone with a sweet tooth who is trying desperately to cut sugar - just not right.

In this case, a credit limit increase is certainly damaging. And this gets to the heart of the Citizens Advice study. It's not really that credit limit increases are a bad thing for all consumers - but protections need to be put in place to protect those who are at risk of falling into a long-term debt problem.

Citizens Advice Recommendations

As part of the Stuck in Debt study, Citizens Advice is recommending four credit-card industry changes to help people stay on top of their finances. These changes center around making sure customers actually want and can afford a credit limit increase, as well as protections to help with debt repayment.

- Credit limits should only be increased when specifically requested by a customer

- In addition to credit history checks, lenders should also conduct Affordability Checks before raising a credit limit

- Credit card firms should offer forbearance to customers who've paid more in charges than capital over 2 years

- Increase minimum monthly payments so that customers pay off their balances sooner

Are You Struggling?

What is meant by “struggling with debt?” In their research, Citizens Advice considered someone to be struggling if they:

- Are in arrears,

- Have missed repayments on a credit or store card,

- Say they find meeting debt repayments a struggle

- Or find their debts to be a heavy burden

If you or someone you know is struggling, it can be very helpful to put a household budget into place. You can find more information and help at Citizens Advice.