Barclaycard Initial Credit Card Review

Barclaycard Initial Credit Card Review

Good for

- Improving Credit

- Individuals with Low income

- No annual fee

- Free text/email alerts

- Free access to Experian

- The chance to lower your interest rate

Bad for

- Those wanting a low interest rate

- Carrying a balance month to month

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

The Barclaycard Initial is no longer accepting new applications. See the Barclaycard Forward credit builder card instead.

If you're looking for a credit-builder card, we recommend you consider the Barclaycard Initial Credit Card. Ideally suited to those looking for their first credit card or those with a poor credit history, cardholders who pay at least the minimum payment on time each month and stay under the credit limit can see their interest rate drop by 5% over two years while improving their credit rating.

Barclaycard Initial Credit Card Review

The Barclaycard Initial is a solid credit card for those with a weak credit history, low income, or looking for their first credit card. This is a good card from a reputable company, useful for individuals trying to build up their credit file. As a credit-builder card, the Barclaycard Initial card's interest rate is higher-than-average, so try to pay down as much of the balance each month as you can manage. In fact, paying the whole outstanding on time each month means you won't incur any interest charges at all.

You can find the likelihood you'll be accepted before you apply by using Barclaycard's eligibility checker, which only leaves a soft search on your credit file. (A soft check doesn't leaves a note on your credit history that you can see, but doesn't leave a mark visible to other potential lenders. Generally, it's good to limit the number of hard searches on your report, as these are visible to other potential lenders. Hard searches occur when you submit an application for a credit card.)

While this card is for imperfect credit histories, you're more likely to be accepted if you meet certain requirements, such as you:

- Are over 18

- Earn over £3,000 a year

- Are employed

- Haven’t been made bankrupt in the last six years—including having an IVA or Debt Relief Order

- Do not have more than one County Court Judgement

- Have lived at their current address for at least three months

- Haven't recently missed a bill payment

Bottom Line: The Barclaycard Initial Credit Card is a solid credit building card that will consider applicants with low income, poor credit or limited credit history. Free access to Experian can help you track your credit rating for improvements and sets the Initial apart from other credit builder cards.

Barclaycard Initial Benefits & Features

| Barclaycard Initial Credit Card Features | |

|---|---|

| Credit Limit | minimum £250 |

| Interest Rate Reduction | By paying at least the minimum ontime each month and staying under your credit limit, your interest rate should drop within 12 months |

| Free Ongoing Access to Experian Credit Score | To help you stay on top of your credit score |

| Free Mobile App | |

| Free Text/Email Alerts | To help you stay on top of your account |

| Eligibility Checker | To see your odds of being accepted |

| Annual Fee | £0 |

| APR | 34.9% variable APR on purchases, cash withdrawals and balance transfers |

Using Abroad for purchases: If you use your Initial card abroad, your purchases will be subject to a 2.99% non-sterling transaction fee. Those looking for a credit-builder card to also use abroad should consider the Aqua Advance Credit Card because it doesn't charge FX fees on non-sterling purchases.

Cash Withdrawal Fees: Using your card to take pounds from an ATM will incur a 2.99% fee, subject to a £2.99 minimum. This means that all withdrawals under £100 are charged a flat rate of £2.99, regardless of withdrawal amount.

Non-sterling cash withdrawals are, again, treated differently. While there is no "cash fee" on foreign currency cash withdrawals, all non sterling transactions (e.g., cash and purchases) are subject to a 2.99% fee (no minimum). The following table illustrates the cash fees and interest treatment for both sterling and non-sterling withdrawals.

| Cash Withdrawal Type | Fee | Interest Free Period (Grace Period) |

|---|---|---|

| Sterling | 2.99% fee (£2.99 minimum) | None (interest charged immediately) |

| Non-Sterling | 2.99% (no minimum) | Yes (if entire main balance paid by next due date) |

Interest on Cash Withdrawals: Withdrawing cash with a credit card is, generally speaking, an expensive way to get money and we don't recommend it. Using the Barclaycard Initial to withdraw cash, say from an ATM, your variable interest rate will be 34.9% APR (variable) regardless of currency. Interest is charged a bit differently, however, depending on whether you are withdrawing pounds or a foreign currency abroad. Cash withdrawals made abroad in a foreign currency are treated to a grace period (maximum 56 days), similar to the grace period offered on purchases—that is, you will not be charged interest on non-sterling cash withdrawals IF you pay your entire main balance (plus any existing monthly purchase plan payments) by the next due date.

Sterling withdrawals, on the other hand, do not get a grace period on interest. For these transactions, interest starts accruing immediately. That is, even if you make your next payment on time, you'll still see an interest charge on your bill reflecting the time from the transaction date until the main account is paid in full.

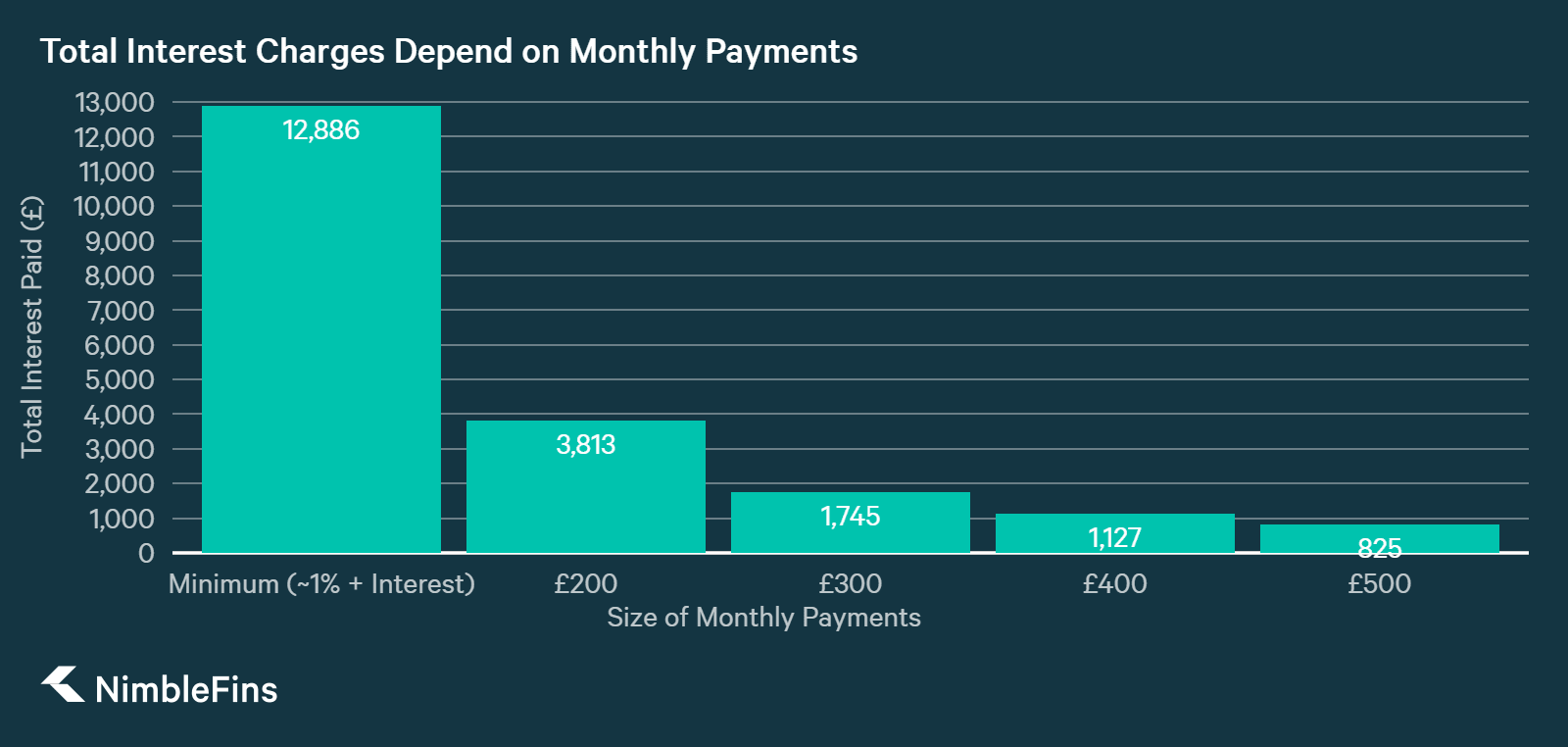

Monthly Payments: Barclays stresses the importance of paying at least the minimum amount due each month in order to improve your credit rating—in addition to paying on time and staying within your credit limit. While this is a valid point in terms of credit history improvement, we'd like to point out the importance of paying more than the minimum amount due each month.

Paying the minimum amount only, it would take around 30 years to pay back the original £5,000, plus you'd pay over £12,000 in interest along the way. A better option, if you are able, is to increase your monthly payments over the minimum required by the credit card company. By paying more per month, not only is the debt paid back sooner but less interest is charged along the way. The following chart illustrates the total interest you'd pay on a £5k starting balance at 34.9%, as a function of the size of monthly payments.

How does the Barclaycard Initial Card Compare to Other Credit Cards?

To better understand the value of the Barclaycard Initial Card you need to look at it in the context of other available options. We compared this card to other similar cards so you can see which may be more suitable for you.

Barclaycard Initial Card vs Marbles Credit Card

The Marbles Credit Card is another good credit card for those with an imperfect credit history; even those with CCJs or bankruptcy in their past will be considered. Marbles also offers a soft credit check eligibility checker before you apply—the FastCheck eligibility checker lets you see your likelihood of being accepted without leaving a mark for other lenders to see. Cardholders can benefit from text reminders and credit limit increases for proper account management.

Quick Takeaway: If you don't meet the Initial's eligibility requirements, the Marbles card can be a solid alternative to get your credit back on track.

Barclaycard Initial Card vs Aqua Reward Credit Card

The Aqua Reward Credit Card is a great card for travelling abroad and earning rewards, all while improving your credit. Cashback is earned at a rate of 0.5% on spending, and the card won't charge any foreign transaction fees.

Quick Takeaway: If you travel frequently, the Aqua Reward card comes with two great perks for credit builders: no FX fees and 0.5% cashback rewards.

Barclaycard Initial Card vs Vanquis Card

The Vanquis Credit Card is another popular UK credit builder card. Unfortunately you need to pay for text reminders on the Vanquis card. If you don't think you need text reminders, this may not be an issue for you. Some cardholders may like the Repayment Option Plan —for a monthly fee, you can access features designed to protect your credit score, like the ability to miss a payment without repercussion or freeze your account without incurring any interest or making any payments—but it's not cheap at a cost around 1.2% per month.

Quick Takeaway: If you meet the eligibility requirements on the Initial, it has more features such as free text alerts and access to Experian. If you can't get an Initial card then the Vanquis may be a viable option.