The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Is Growth in 0% Purchase Cards Good or Bad for Consumers?

Back in 2017 and 2018, credit card companies were in a virtual horse race, increasing the length of their 0% purchases and balance transfer periods. The longest no-interest periods extended up to around 40 to 43 months for balance transfers and 29 to 31 months for purchases, with many offers of those lengths to be found in the UK market.

Since then, 0% promotional periods have been steadily dropping. By early 2020, the longest 0% promotional periods were 27 months for purchases and 29 months for balance transfers.

At first glance, credit cards that charge 0% interest for a longer period sound like a good deal for consumers. After all, paying 0% is surely better than paying 18.9%, or more. But are these 0% promotional offers good or bad for consumers?

Buying What We Can’t Afford

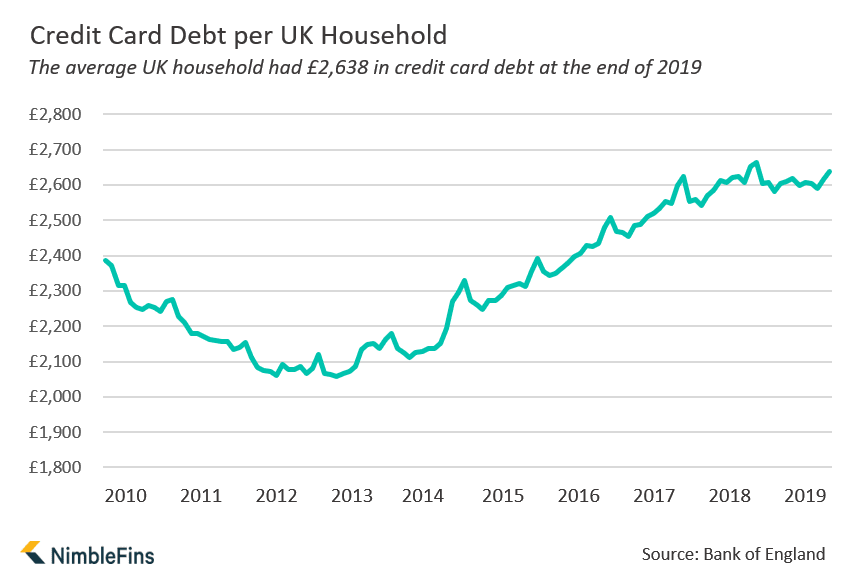

Credit card debt is nearly at a record high in the UK—according to the latest figures from the Bank of England, credit card lending grew to £73.4 billion in December 2019, up £645 million in the month. This figure equates to over £2,600 of credit card debt per UK household.

Credit card lending accounts for a third of average unsecured credit lending in the UK (excluding student loans), which stands at over £7,850 per household. Much of this lending is in the form of 0% purchases cards.

Trouble can start when consumers use a 0% card to make purchases they can't pay off by the end of the promotional period. And without monthly interest payments to pay, cardholders may be comfortable carrying higher levels of debt than they would normally. If care isn't taken, personal debt levels can creep higher and higher.

Losing Your 0% Interest Promotional Period

Care must be taken not to lose the 0% promotional period. Consumers can really end up in a bind if they are depending on 0% interest but the promotion comes to a premature and they revert to the stated interest rate on the card.

How can you lose a 0% interest promotion? By missing a monthly payment or exceeding the credit limit during the promotional period. Doing so violates the terms of most cards and brings the 0% period to a premature end. One little mistake and you’ll be stuck paying the stated rate on your remaining balances[symbol:@m-dash]easily 19.9% but your rate could be 2X or 3X as high as that.

Credit card companies don’t make money during 0% interest periods[symbol:-m-dash]they lose money because they're lending money for free. How do they make this up? When cardholders pay interest or fees.

Since issuers are continuing to hand out 0% interest cards like there's no tomorrow, it’s a sure bet that lots of cardholders are either violating the terms of their promotional periods (so they lose the 0% promotion and pay their stated interest rate) and/or carrying balances beyond the promotional periods—in either case, consumers can end up paying at least 18.9% interest on their "0%" cards.

Balance Transfer Cards Have the Same Problem

Borrowing face a similar issue with balance transfer cards if they don't make their payments on time or exceed the credit limit. Additionally, cardholders won't get a 0% rate if the balance isn't transferred within a window that's usually 60 or 90 days from account opening.

Can a 0% Card Ever be Beneficial?

There are, of course, circumstances when a 0% card can be useful. Perhaps the boiler conked out, the car broke down and the children need new shoes—all in one month. In these cases it can be helpful to get a few months of breathing space where you are making monthly payments, but they're going strictly towards paying down your debt, not interest charges.

In short, 0% cards can be useful for consumers who use them to actively improve their personal finances (e.g., reduce their debt levels). But for consumers who use promotional periods to keep on shopping while postponing debt repayment, 0% cards with longer and longer promotional periods can be bad news indeed.