Lloyds Bank Platinum Credit Cards: The Balance Transfer Offer for You?

Lloyds Bank Platinum Credit Cards: The Balance Transfer Offer for You?

Good for

- Reducing interest charges on existing credit card debt

- Reducing interest charges on purchases

Bad for

- Those wanting to move debt from another Lloyds credit card

- Anyone wanting to check eligibility before they apply

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

If you're paying interest on existing credit card balances, the Lloyds Bank Platinum Credit Card is a suite of balance transfer offers to help you reduce interest payments and eliminate debt sooner. The suite of cards ranges from a no-fee, shorter 0% interest period up to a larger-fee, longer 0% interest period on balances transfers. How does the card compare?

- Lloyds Balance Transfer Credit Card Offers

- Lloyds Balance Transfer Features

- How Much Can I Save with a Balance Transfer Credit Card?

Lloyds Bank Platinum Credit Card Balance Transfer Review

The Lloyds Bank Platinum Credit Card is a group of cards whose primary function is balance transfers. If you're paying interest on an existing balance on another card, moving that balance to one of Lloyds' balance transfer cards may save you hundreds or even thousands of pounds by reducing your interest payments.

The Lloyds Bank Platinum Credit Card offers a selection of balance transfer offers that differ primarily in the length of time a cardholder pays 0% interest on balance transfers. Generally speaking, a longer 0% intro period means a higher balance transfer fee. This is not surprising, since the bank has to charge for the additional risk of taking on your debt for a longer time.

Over time, the balance transfer durations (the time you get a 0% grace period) have come down significantly, along with the market. In 2018, the no-fee offering was 25 months; in 2020 it was down to 15 months. And the longest balance transfer on offer dropped from 35 months in 2018 to 28 months in 2020.

As we enter January 2026, the balance transfer market has expanded significantly to meet rising consumer demand. The longest 0% period currently available has reached a record 38 months (offered by TSB). Specifically, Lloyds Bank has remained highly competitive, currently offering a 33-month 0% period with a 2.49% fee, providing nearly three years of breathing room for those consolidating debt.

Offers change regularly, so it's best to check their website (you can use the "Apply Now" button above) to see the latest offers right from the horse's mouth.

Note: Lloyds may offer up to 49% of applicants a shorter 0% duration.

Bottom Line: Lloyds Bank Platinum credit card balance transfer offers are generally competitive, but be aware that you may get a shorter-than-advertised 0% period. Be sure to pay your minimum payment on time, or you'll lose the 0% intro rate.

Lloyds Balance Transfer Card: No Fee 0% Balance Transfer

In a welcome shift for consumers, 'no-fee' balance transfer cards are widely available again in early 2026. While Lloyds offers various tiered options, the market's leading no-fee deals—such as those from Sainsbury's—now offer up to 22 interest-free months. This makes them a viable alternative for those with smaller balances who want to avoid the upfront percentage charge.

Lloyds Balance Transfer Card: Low Fee and Longer 0% Period

If you need a bit more time to bring your credit card balances down without incurring interest charges, you can consider the Lloyds' Low Fee 0% offer. This slightly longer promotional period will cost you a bit more in terms of the transfer fee charged on all initial transferred balances than the "no fee" card. New purchases made on the Low Fee card also benefit from no interest period on purchases.

For consumers needing a longer 0% period, we think this Low Fee deal is Halifax's best offer (it ends up being cheaper than the Longest 0% deal, discussed below, due to the balance transfer fees).

For those prioritizing the longest possible window to clear a large debt, the primary 'low fee' benchmark for Lloyds in early 2026 is 33 months at 0% interest with a 2.49% transfer fee. While the fee is slightly higher than historical lows, the extended nearly three-year duration provides a crucial buffer against the high-interest environment.

Lloyds Balance Transfer Card: Longest 0% Period

Lloyds' Longest 0% Period offer gives more time to pay back balances, but the higher fee on initially transferred balances may not be worth it if you don't need the time. If you can manage with a slightly shorter time at 0% APR then we recommend considering the Low Fee offer, above, because you might pay a lot less in fees.

In January 2025, Lloyds was offering a 33 month balance transfer credit card; while not market leading (other cards offer up to 38 months at the time of writing) it may be long enough for some people. And it comes with a lower transfer fee (2.49%) compared to the longest cards (up to 3.49%).

Top Tip

We want to reiterate how important it is for all balance transfer cardholders to pay off their outstanding balance within the 0% APR promotional period. Also, it is crucial to stay within your credit limit and to make your minimum monthly payments on time in order to keep the promotional offers. Punctuality is vital in 2026: missing a payment can cause your 0% rate to 'shoot up' to the normal APR on your card, which is likely to be in the low 20% range for half of people.

Can I Hold More than One Lloyds Bank Credit Card?

Like most other credit card companies, Lloyds doesn’t let you transfer a balance from one of their own credit cards. This doesn’t preclude current Lloyds customers from opening a new Lloyds balance transfer card. Lloyds does permit consumes to hold a second Lloyds Bank credit card (subject to the conditions, below, from their website):

- You don’t already have a Classic or Student credit card with Lloyds Bank.

- You can only have one Rewards credit card account, even if the second Rewards card you want to choose is different to your existing Rewards card. The Rewards credit cards we currently offer are Avios Rewards, Premier Avios Rewards and Choice Rewards.

- You can only have a maximum of two credit cards with Lloyds Bank, and a maximum of five with the Lloyds Banking Group (which also includes Halifax and Bank of Scotland).

- You’re not applying within 60 days of having opened your first credit card with Lloyds Bank.

- Your application is subject to a full credit check.

What is a Balance Transfer Credit Card Good For?

A balance transfer credit card is meant to help consumers manage their credit card debt, by placing the debt onto a special credit card that doesn’t charge interest for a time. This no-interest situation not only can save consumers money, but consequently allows them to pay off their debt sooner—if used properly.

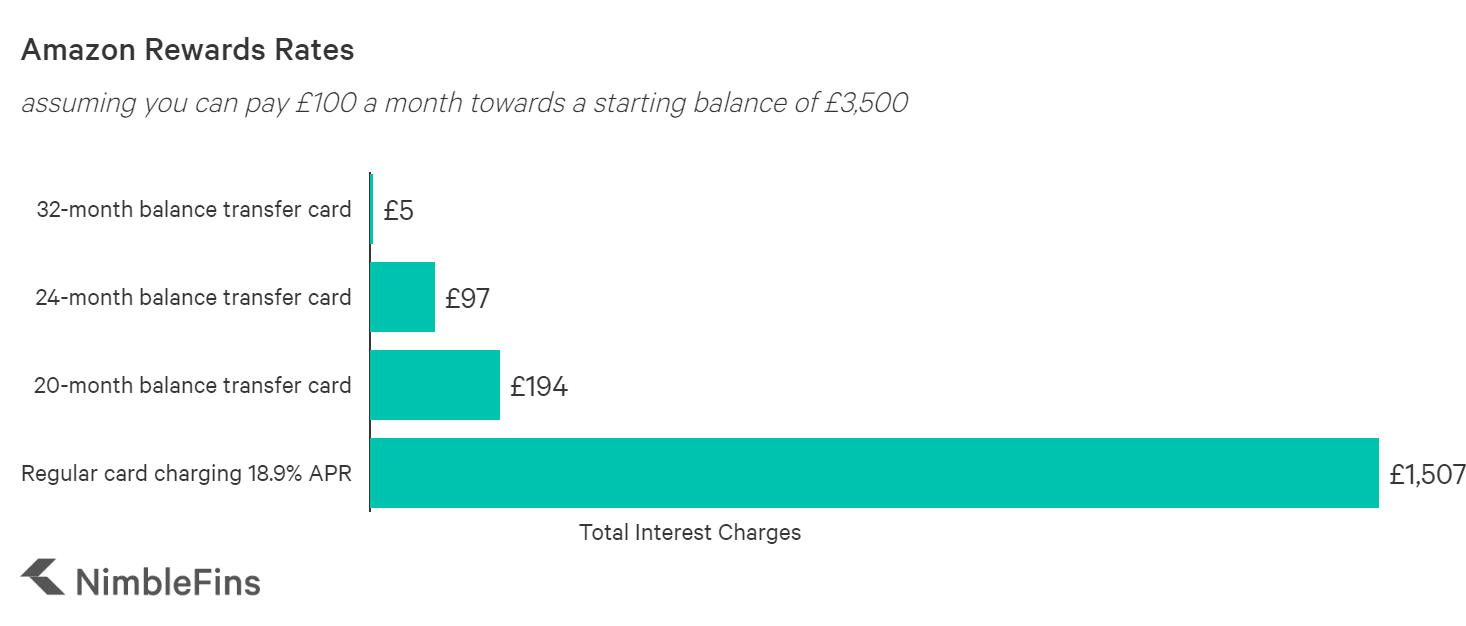

Imagine you have a balance of £3,500 on a credit card that is charging you 18.9%. Assuming you don’t purchase anything else with the card, and can make monthly payments of £100, it will take you 51 months to pay off this debt. Along the way you will have paid over £1,500 in interest. Moving this debt to a 0% APR balance transfer card of suitable duration, you can save this £1,500 in interest and be debt free sooner.

Even choosing a balance transfer with a too-short duration can still be beneficial. The following chart shows how much interest you would pay in total on 5 different credit cards, assuming you can manage to pay £100 a month towards a balance of £3,500. Even if the 0% period ends up being too short for you, a balance transfer can still be beneficial relative to a card charging 18.9%.

If your credit card charges 24.66% (the current average at the beginning of 2026), the interest charges would by over £2,450.

Understanding the 2026 Debt Landscape

The importance of these balance transfer tools is underscored by the current scale of UK household debt. As of early 2026, the average UK household debt (excluding mortgages) has reached £18,392, with credit card balances alone averaging £2,601 per household. With debt levels at these heights, even a small reduction in interest rates can have a massive impact on a family's monthly disposable income.