The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Credit Card Lending Rises Again: Top Tips to Reduce Credit Card Interest Charges

According to recent NimbleFins of data from the Bank of England, credit card lending has grown significantly, with the average credit card debt per UK household reaching £2,601 in 2025. In the face of these rising debt levels, the cost of borrowing has also surged; as of January 2026, the average credit card interest rate (APR) in the UK reached 24.66%, the highest in over 30 years. This record high makes it more important than ever for consumers to take proactive steps to minimise interest charges.

Basic Credit Card Rules

Pay (at least) your minimum monthly payment on time every month and stay within your credit limit. Breaking either of these means you'll incur default charges, you may be reported to credit agencies and your interest rate may subsequently rise. All of these are counterproductive if you're trying to save money on interest charges on your credit card!

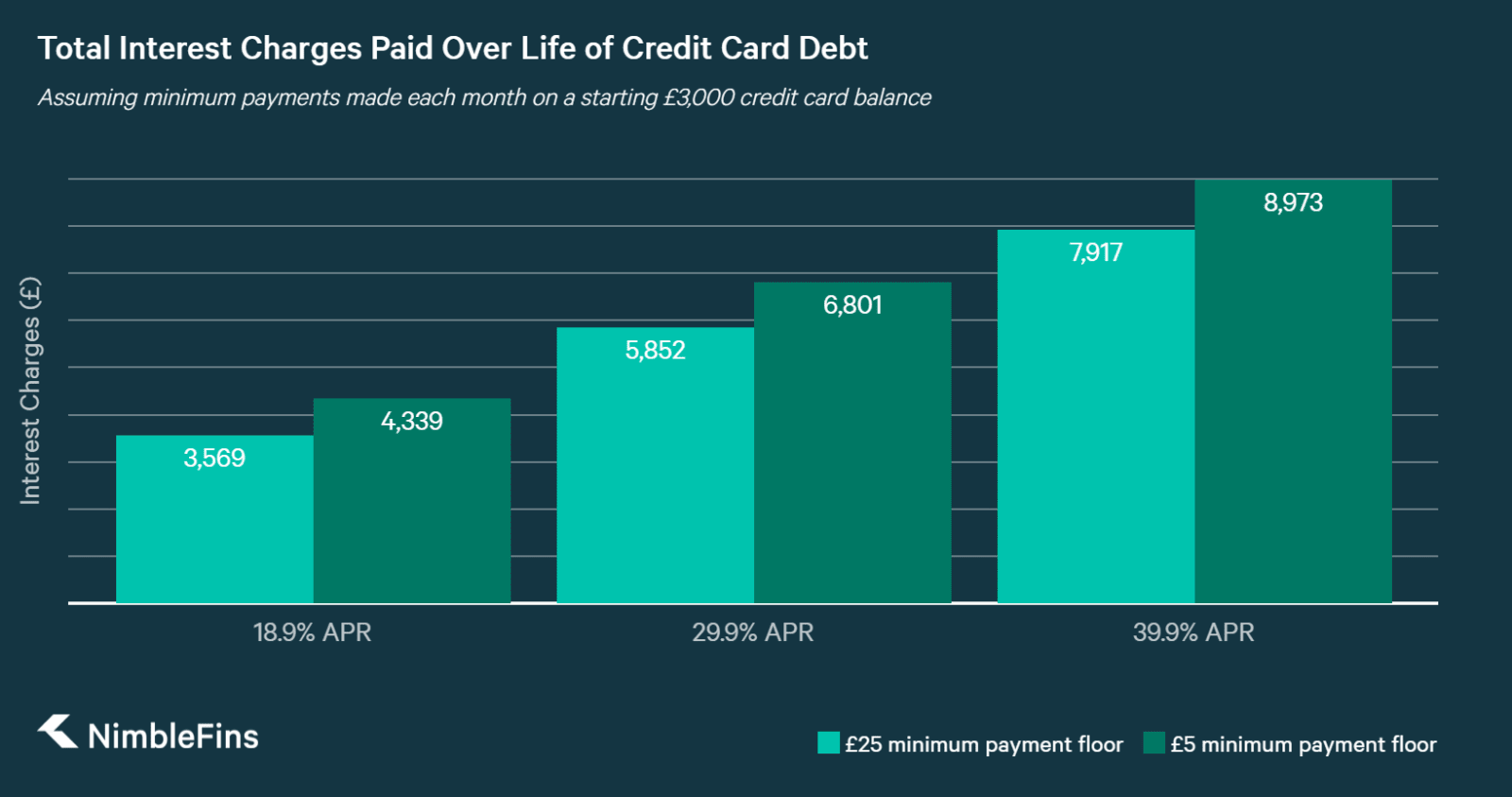

However, be aware that for many modern credit cards, the minimum payment floor is typically between £5 and £25 (or a percentage of the balance plus interest). With the current 24.66% average APR, paying only the minimum requirement on a typical balance can trap you in debt for years, as the vast majority of your payment is swallowed by interest charges rather than clearing the principal balance.

Pay as Much as You Can

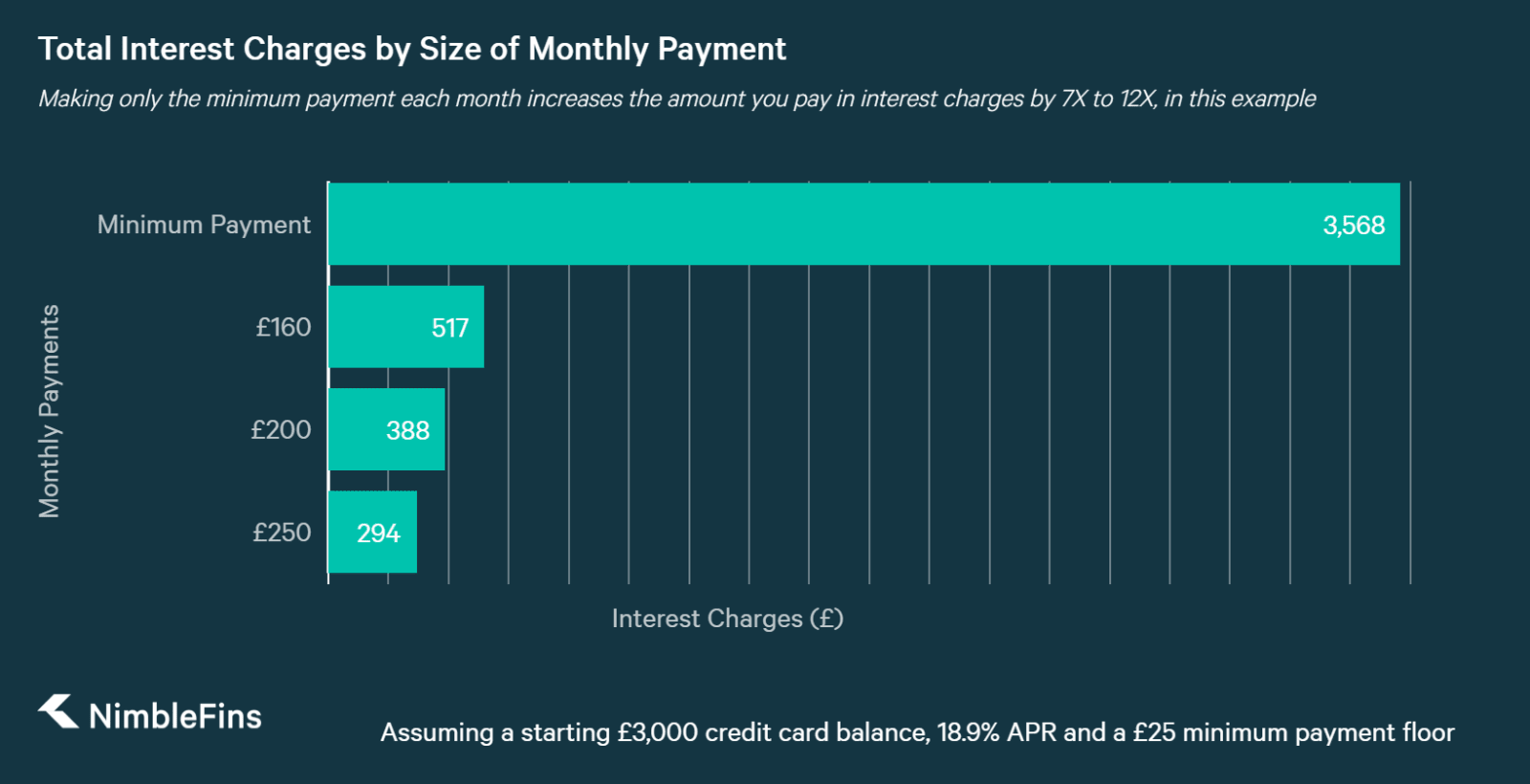

Whatever the interest rate, make your monthly payments as large as possible. Paying at least the minimum amount due is certainly critical to keep promotional periods and avoid charges and being reported to the credit agencies. However, those paying only the minimum amount each month will typically pay interest charges amounting to 1.5X to 3X their original debt (depending largely on the interest rate and the minimum payment floor), as you can see in the following chart.

Most people aren't aware of the minimum payment floor on their credit card, but it's really important—especially if you only pay the minimum each month. The "floor" is a £ amount and is a lower bound for the minimum monthly payment calculation. The floor comes into effect towards the end of debt repayment, when your balance is so low that the calculation returns an amount lower than the floor. You don't pay this lower amount, you pay the floor.

Basically, a higher floor means you'll pay back the remaining balance sooner (because you're paying more to the credit card company each month once the floor kicks in); a lower floor means a longer time to pay back your debt and more interest charges along the way.

By making monthly payments larger than the minimum amount due, cardholders can pay much less in interest charges over time. Why? The extra you pay each month goes wholly to reduce your debt (not towards interest), enabling you to reduce the outstanding debt sooner.

Promotional Rules

If purchases were made on a 0% interest card, be absolutely sure to pay on time every month, pay at least the minimum amount due and stay within your credit limit. Failure to do so usually means the 0% promotional period is brought to an early end—which means your purchases incur interest charges at your card’s standard interest rate (typically 19.9% or more) going forward.

The same also applies to balance transfers on 0% credit cards—pay at least your minimum monthly payment on time each month or else you'll lose the 0% promotional and start paying your stated rate on transferred balances.

Pay Off Debt within Promotional Periods

In fact, those with a 0% card should try to pay back their full balances before the 0% promotional period ends, thereby eliminating interest charges altogether on that debt.

Switch to a Balance Transfer card

Those with debt on an interest-bearing card may be able to move their balance to a 0% balance transfer card. This strategy can certainly be a good way to reduce or even eliminate interest charges. But only if you follow the rules mentioned above (pay at least the minimum each month on time and stay under the credit limit!). And remember, a new credit card application will leave a mark on credit record, so take this into consideration before you apply.