The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Rising Risks for Credit Card Borrowers

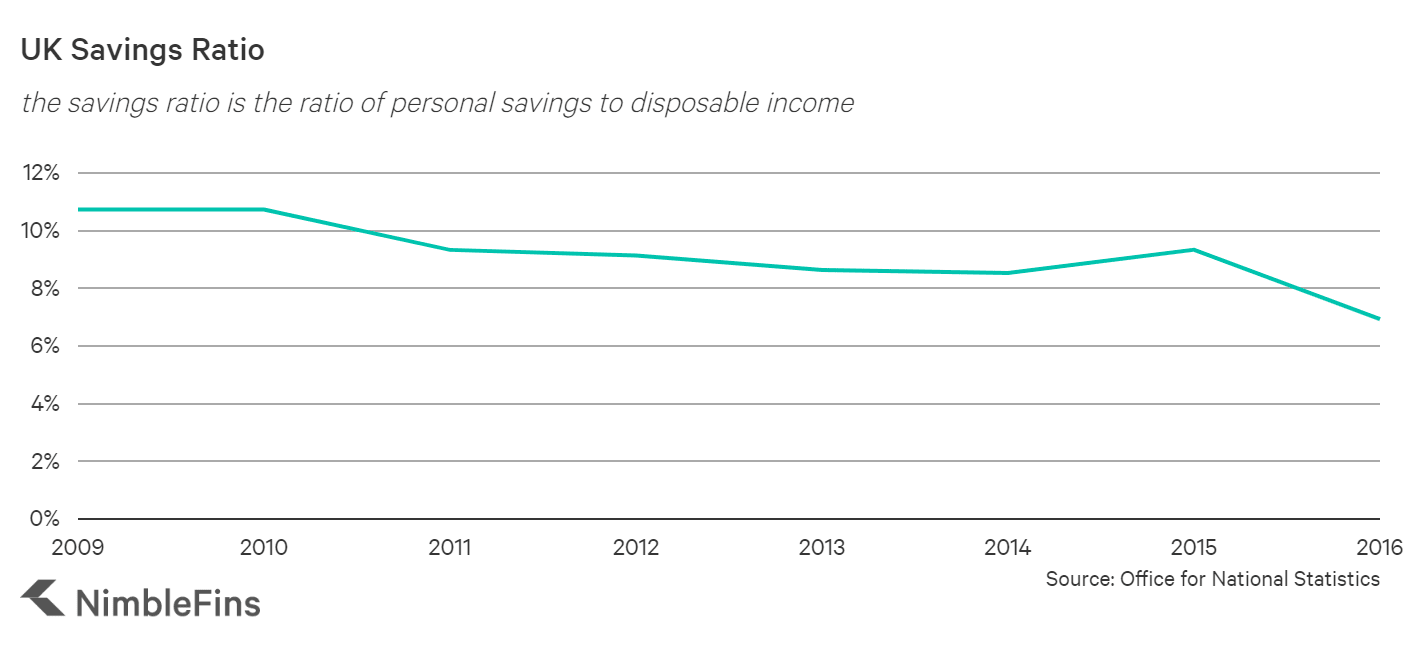

The Office for National Statistics (ONS) has recently announced that the UK Savings Ratio has dropped to 6.9%, which means households have savings representing just 6.9% of their disposable income. This savings figure is particularly alarming when taken alongside the continued rise in credit card lending.

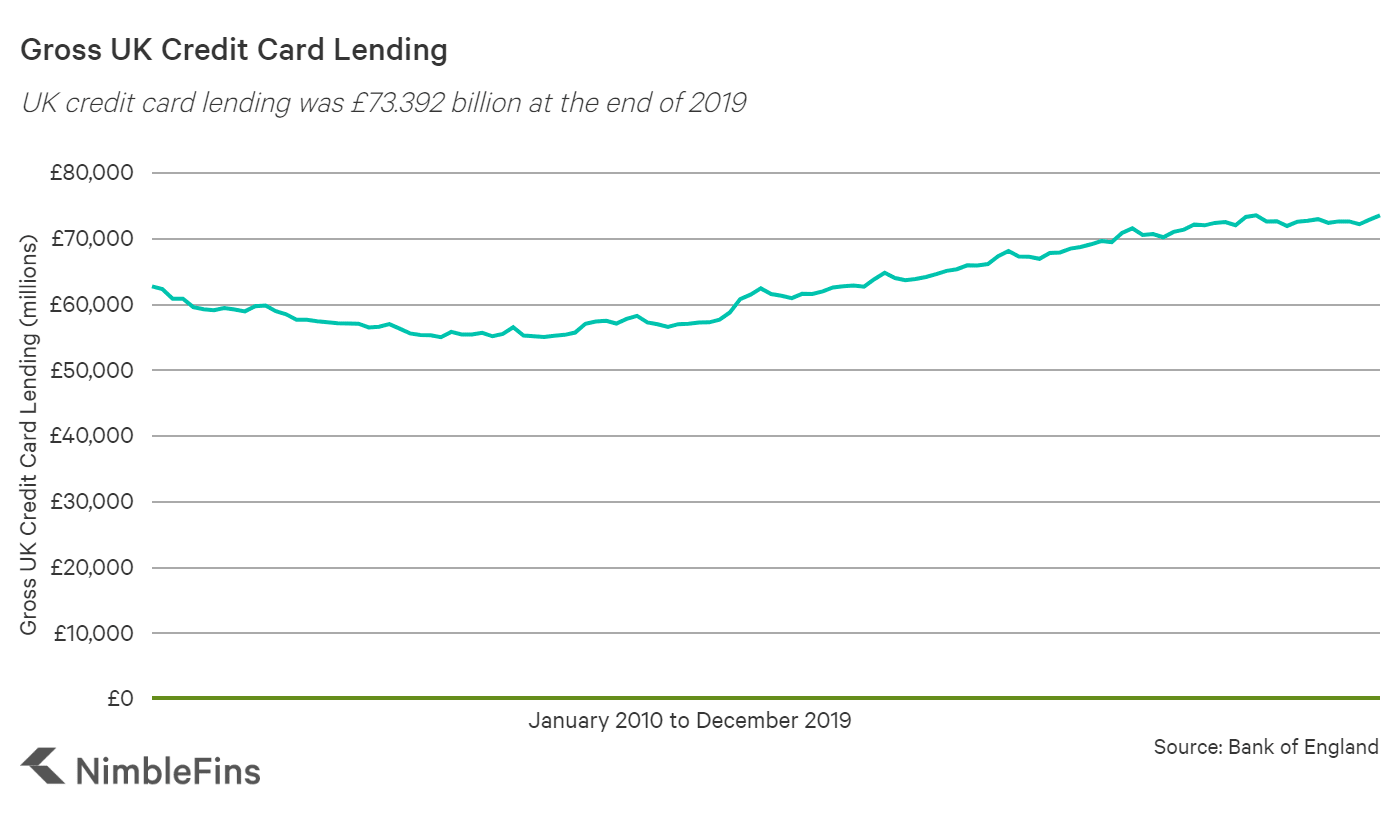

Rise in Credit Card Lending in the UK

Credit card lending rose yet again, hitting a new high of £73.392 billion as of 31 December 2019. Credit card balances are a significant source of household debt in the UK, and the trend of increased credit card lending continues.

Many consumers delay paying back credit card debt by taking advantage of 0% interest purchase and balance transfers deals. While these tools can be useful for customers to pay back debt without interest charges, they can result in consumers carrying debt for longer if the debt just gets moved from card to card. As we discussed in our article Is the Growth in 0% Purchases Cards Good or Bad for Consumers, longer 0% periods are not always beneficial.

UK Savings Ratio

Savings are important to carry households through unexpected financial stress such as being made redundant or unexpected bills. The Money Advice Service recommends you have at least 3 months of expenses saved up. Using data from the ONS, we found that the average household spends £529 per week on expenses like food, housing, transportation, entertainment, etc.

To cover 3 months of spending, the typical UK household should therefore have over £6,300 of savings tucked away. As the savings ratio dips lower and lower, fewer households will find themselves with enough savings.

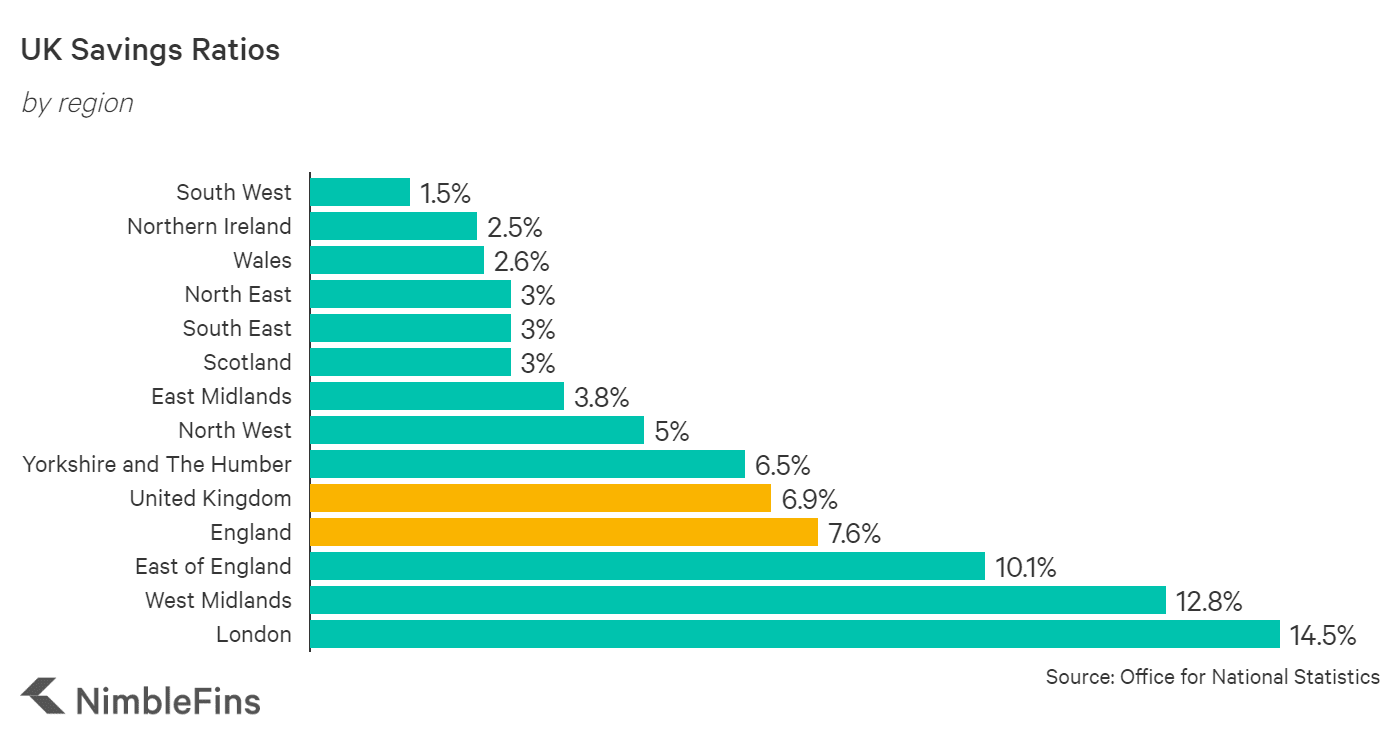

Savings Ratios by UK Region

Savings rates vary drastically by UK region. London has the highest savings ratio, at 14.5%. The South West has the worst savings ratio at just 1.5%.

| South West | 1.5% |

| Northern Ireland | 2.5% |

| Wales | 2.6% |

| North East | 3.0% |

| South East | 3.0% |

| Scotland | 3.0% |

| East Midlands | 3.8% |

| North West | 5.0% |

| Yorkshire and The Humber | 6.5% |

| East of England | 10.1% |

| West Midlands | 12.8% |

| London | 14.5% |

| England | 7.6% |

| United Kingdom | 6.9% |

Taken together, these lending and savings statistics are a worry. With less money saved up in the bank, consumers finances are more vulnerable. Without a savings buffer, any loss of income or unexpected bills can make existing credit card monthly payments even more difficult to make, potentially resulting in costly fees and higher interest rates as discussed in our article about how balance transfers work. Hand in hand, rising credit card lending and a lower savings ratio can be a recipe for financial disaster.