The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Why you REALLY Shouldn't Carry Debt on a Credit Builder Card

Credit cards are a notoriously expensive way to borrow. The potential costs are even greater for those who struggle with debt, have a weak credit score and hold a credit builder card, due to higher than average APRs of 30%, 40% or more on cards for bad credit.

While credit card companies may benefit financially from your paying high interest charges each month for your borrowing, YOU are far better off by paying down the full balance each month. Learn why you should only make charges to a credit builder card that you can repay in full by the due date. We'll explain the potential costs and ramifications of carrying a balance on a credit builder card to help you manage the balance on your credit builder card to your advantage.

Interest Payments

Since interest rates are higher on credit builder cards, carrying a balance means you're losing money by paying interest charges. The average variable APR on credit cards for bad credit is 36%—2X the average credit card APR, and 4X what someone with great credit might pay on a low rate card. The effect of high interest rates can have a massive impact on your finances, especially if you're working to improve your financial situation. Paying interest simply means less money in your pocket at the end of the day.

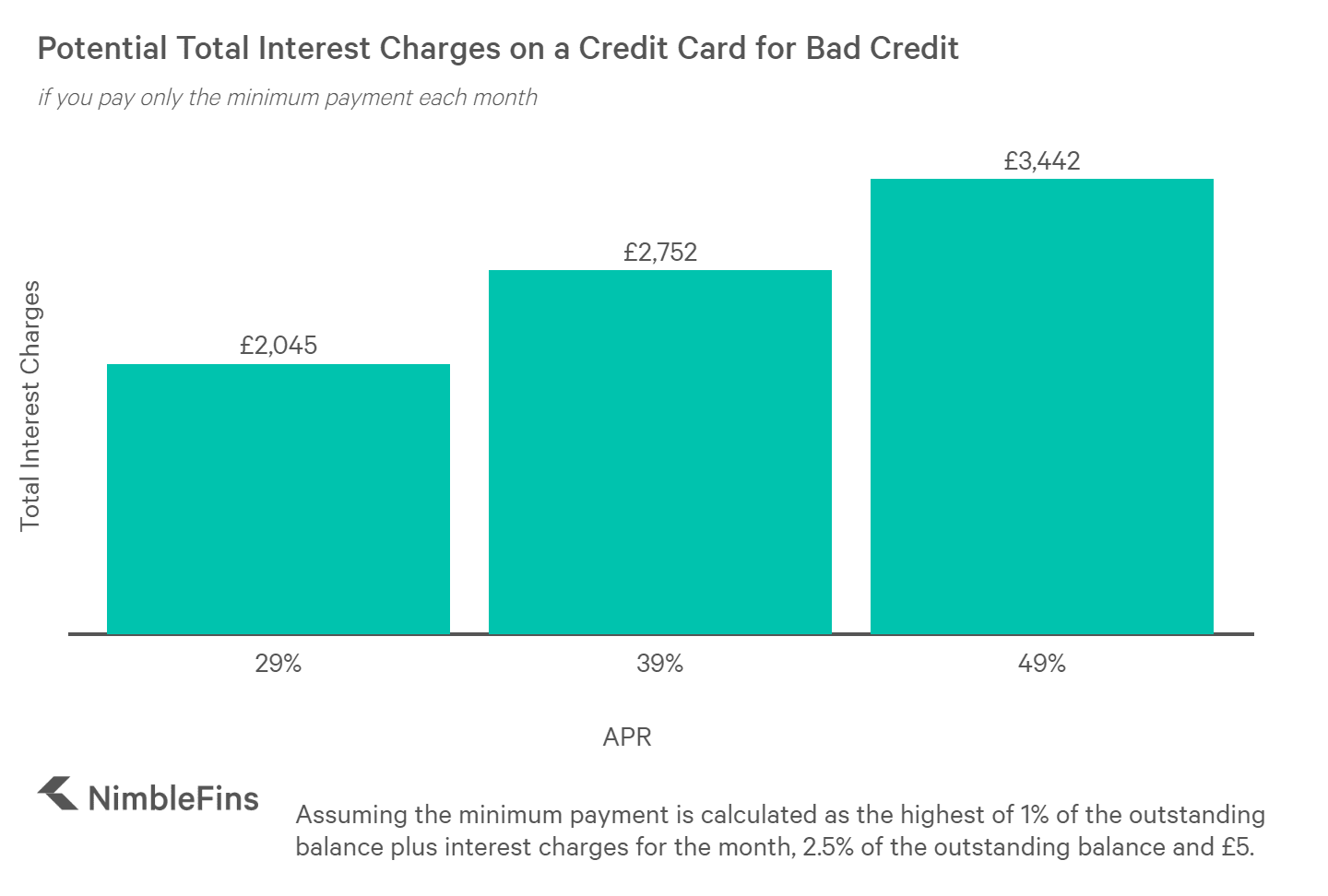

By paying the full balance by each and every due date, on time, you won't pay interest. To understand how valuable it can be to pay back all your purchases each month (e.g., not carry a balance from month to month), it helps to understand how much in interest charges you will avoid by doing so. Let's look at an example of a £1,000 purchase made on a card with different APRs and a £5 minimum payment floor, for which only the minimum payment is made each month. As you can see, a cardholder who originally borrowed on a high-interest card can easily pay 2X, 3X or more of their original purchase in interest charges.

Total Interest Charges on £1,000 of Purchases: Cardholder makes Minimum Monthly Payments Only

| APR | Total Interest Charges over Time |

|---|---|

| 29% | £2,045 |

| 39% | £2,752 |

| 49% | £3,442 |

To the extent you can pay back your full balance each month instead of only paying the minimum each month, you can avoid these charges. For every £1,000 of purchases, you can save £2,000, £3,000 or more depending on the APR.

The Difference £20 a Month Can Make

What if you just can't pay the full balance back? Paying as much as you can manage can still help. For example, paying an extra £20 each month on a 39% APR credit card (above the minimum monthly payment that is required) can save you nearly £2,200 in interest charges over time on a starting £1,000 balance.

| Savings by Paying Extra £20 per Month | Total Interest Savings |

|---|---|

| 29% | £1,624 |

| 39% | £2,196 |

| 49% | £2,755 |

In large part, these massive interest savings come from avoiding the trap of the Minimum Payment Floor through a larger monthly payment.

Credit Score

Carrying a balance from month to month on a credit card, especially if you are near the limit and on a high-interest card, can adversely affect your credit rating. Persistent borrowing from a credit card company can be a sign to lenders that you are struggling to handle your existing debt—otherwise, you'd certainly pay off the balance to avoid paying interest. As a result, carrying a balance on a credit builder card can make it difficult to borrow money in the future, especially at a reasonable interest rate.

Can't You Switch to a Balance Transfer Card?

If you do end up with a balance you can't pay down on a credit builder card, can't you just move it to one of those 0% balance transfer cards that you hear so much about? Not so fast. Those with weak credit scores are often NOT eligible for 0% balance transfer cards. A weaker credit history unfortunately means you present a higher potential risk to the credit card company (e.g., of not paying them back), so you're not likely to secure a 0% deal—lenders need to get reimbursed for taking on the risk of your debt.

What to Do

Credit builder cards certainly have a place in the market. Used wisely, a credit card for bad credit can be a tool to help you rebuild your credit rating—when other credit cards might not otherwise accept your application.

But credit builder cards can be extremely costly if you carry a balance from month to month. If you find yourself struggling to pay back your outstanding debt, you may want to get free debt advice from organizations including the National Debtline, Citizens Advice Bureau and StepChange Debt Charity.

To the extent that your spending outpaces your income, it can help to find ways to reduce spending on Christmas, save money on takeaways, etc.