Aqua Start Credit Card Review: The Easiest Aqua Card to Qualify for?

Aqua Start Credit Card Review: The Easiest Aqua Card to Qualify for?

Good for

- A first credit card

- Receiving free text reminders and credit report

- Credit limit increases

Bad for

- Those wanting a high credit limit

- Individuals looking for a low interest rate

- Those needing to carry a balance from month to month

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Note: The Aqua Start card is no longer available to new applicants. You may prefer to consider the Aqua Classic card as an alternative.

The Aqua Start Credit Card is a basic credit builder card for those with virtually no credit history in the UK. Since it is targeted at this segment of the market, it comes with a higher-than-average interest rate at 49.9% APR and, not surprisingly, doesn't offer any bonuses or rewards.

Aqua Start Credit Card Review

The Aqua Start card is a basic card for those who are new to credit in the UK and can be used as a tool to establish your credit history. The Start is Aqua's entry-level card with the lowest acceptance criteria, and is suitable as a first credit card.

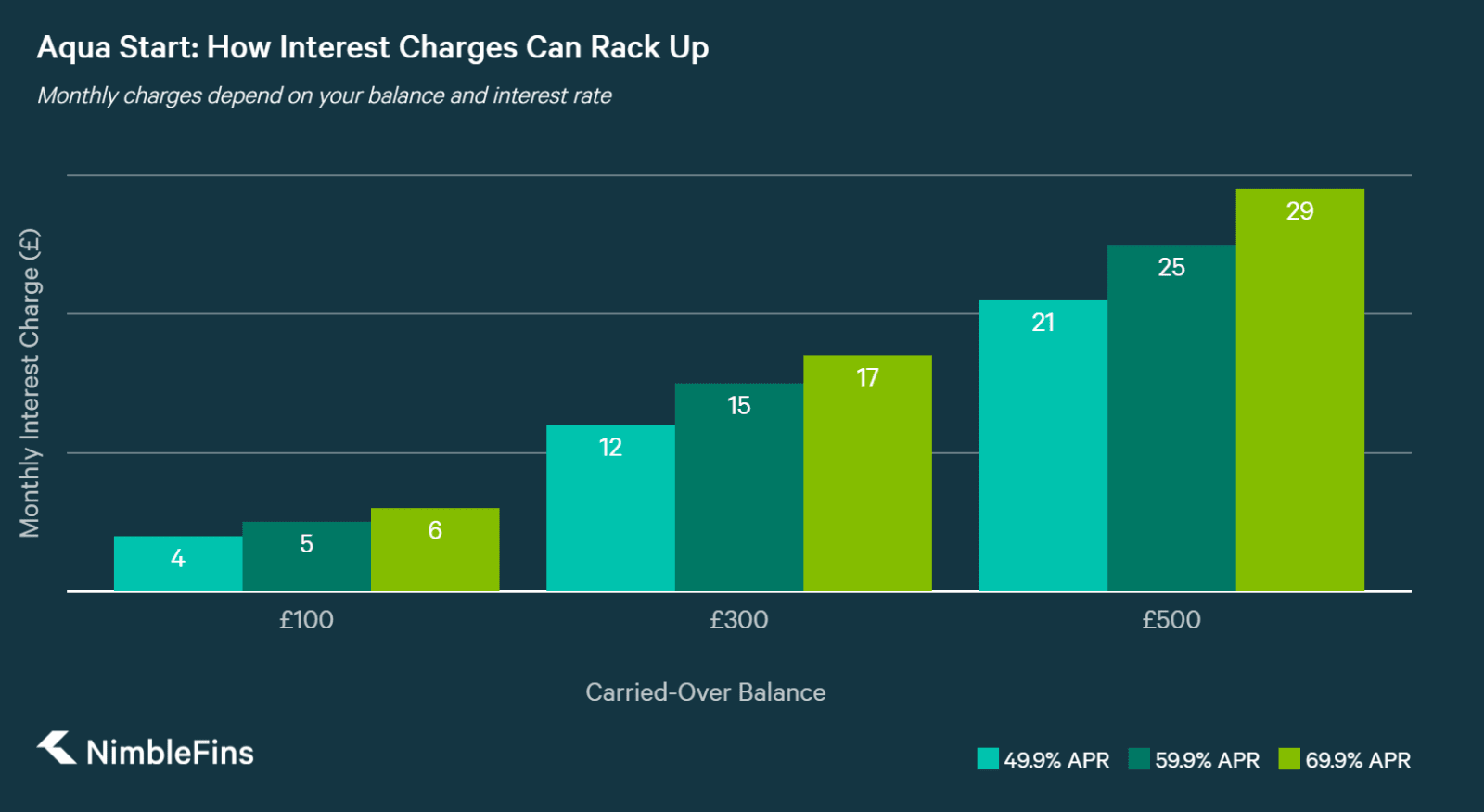

While the Start is attractive in its accessibility to those with no or poor credit, be aware that it carries very high interest rates at 49.9% APR—much higher than average. We recommend using this card to establish a good credit record only—not for carrying a balance from month to month. The high interest rates mean you should, to the very best of your ability, pay down the full balance on time every month. Carrying a balance will result could result in significant interest charges, as you can see in the following chart.

Credit Building: Proper management of this account—by paying on time and staying under your credit limit—can lead to the gradual building of your credit history. Once your credit score has improved, you can apply to a card with lower interest rates or perhaps perks like no foreign transaction fees or rewards—for instance, the Aqua Rewards card or the Aqua Advance for no FX fees if you'd like to stay within the Aqua family.

Bottom Line: Use the Aqua Start card as a first credit card to build a healthy credit history, by staying within your credit limit and always paying on time. Due to higher interest rates, we recommend paying down your full balance every month to avoid significant interest charges.

Aqua Start Benefits & Features

| Aqua Start Card Features | |

|---|---|

| Credit Limit Increases | By staying within your credit limit and making your minimum payment on time, you may be eligible for a credit limit increase every fourth month. |

| Transaction Fees | Non-sterling transaction fees of 2.95% |

| Cash Withdrawal Fee | 3% fee at home and abroad (£3 minimum) |

| Initial Credit Limit as low as | £100 to £300 |

| Text Reminders to help you |

|

| Annual Fee | £0 |

| APR |

|

Some positive features are that you are able to change your payment date to a day that suits you—perhaps just after you get paid—and free access to text reminders. Text reminders can alert you to a statement being ready, that you're nearing your credit limit or that a payment is due. We really like these features, because staying under your maximum limit and paying on time are critical for those trying to establish a good credit history.

Credit Limit: After three months with the card, Aqua may reevaluate your situation. Credit limits start off low on this card, usually around £100. But by properly managing your account (i.e., paying on time and staying within your limit), your credit limit may be raised in your fourth month. Once your credit limit exceeds £1,000, the credit rating agencies should take note of your responsible management of financial obligations.

How does the Aqua Start Card Compare to Other Credit Cards?

To better understand the value of the Aqua Start Credit Card you need to look at it in the context of other available options. We compared this card to other rewards cards so you can see which may be more suitable for you.

Aqua Start Card vs Marbles Credit Card

The Marbles card is a credit card that may accept those with a very limited credit history, or poor credit. Even individuals with CCJs or bankruptcy in their past will be considered. One standout feature is that Marbles is one of the few credit cards offering a soft credit check eligibility checker. Use this FastCheck tool before you apply, to see your likelihood of being accepted without leaving a mark on your credit record for other lenders to see.

Quick Takeaway: While both cards are issued by New Day, the Aqua Start may be better as a very first credit card, as they market it specifically at those without credit history in the UK.

Aqua Start Card vs Capital One Classic Card

The Capital One Classic card is a solid card for those with a bit of credit history in the UK, even if that credit history is poor. A major benefit of this card is that you can check your eligibility before you apply; Capital One’s QuickCheck tool uses a soft search of your credit rating, which doesn’t leave a footprint for other potential lenders to see. Capital One virtually guarantees that your application will be accepted if the QuickCheck tool first indicates acceptance (unless they find certain information of fraud prevention databases or can’t verify your id).

Quick Takeaway: Those without any credit history are more likely to be successful applying for the Start card. Those with some history (even a poor one!) can probably find a lower interest rate with the Capital One Classic.

Aqua Start Card vs Vanquis Credit Card

The Vanquis credit card is open to applicants with no credit history, poor credit history or are unemployed are all considered. Initial credit limits are lower, between £150 and £1,000, with a representative APR of 39.9%. Potential applicants can use the pre-application eligibility checker to see their likelihood of being accepted before they apply (useful to help avoid an unnecessary hard credit check and a rejected application).

Quick Takeaway: The Vanquis card may charge you a lower interest rate (representative APR of 39.9%) and give you a higher initial credit limit, so may be a better fit.